Monthly commentary BMS July 2018

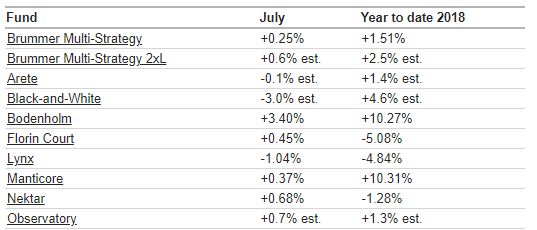

Brummer Multi-Strategy (BMS) increased by 0.3 percent in July, resulting in year-to-date performance of 1.5 percent. Hedge Fund Research’s HFRI Fund-of-Funds Composite Index declined 0.1 percent in July and has returned 0.8 percent year-to-date.

July was to a large extent characterised by extreme weather conditions and continued international trade negotiations, which thus far has weighed more on sentiment than actual production and trade activity. Global equity markets posted gains as earnings season got off to a positive start, with advances in the US and the majority of Europe and Asia. The US and Sweden reported strong economic growth for the second quarter and both US and European interest rates rose. Meanwhile, the US dollar strengthened against other G5 currencies and weakened against several Emerging Markets currencies. In commodities, oil and metals prices declined.

Five of the eight funds in which BMS invests contributed to the positive performance in July. There was no clear relationship between the returns and different focus areas of the underlying investment strategies, once again highlighting the low correlation between the funds. The top performer of the month was the long/short equity fund Bodenholm, which had a strong alpha contribution to BMS. On the negative side of the portfolio, long/short equity fund Black-and-White was the main detractor, primarily due to losses on long positions in the US TMT sector.

Ahead of August, the portfolio managers increased the allocation to the long/short equity funds and reduced the allocation to Nektar and Observatory. As of 1 July 2018, BMS Master invests in Lynx SEK (Bermuda) instead of Lynx (Bermuda). Lynx SEK (Bermuda) has a leverage ratio of two relative Lynx (Bermuda). The risk allocation to Lynx is however largely unchanged. In order to facilitate continued historical comparison, the corresponding underlying allocation and return of Lynx (Bermuda) will be reported.