Brummer Multi-Strategy monthly commentary February 2020

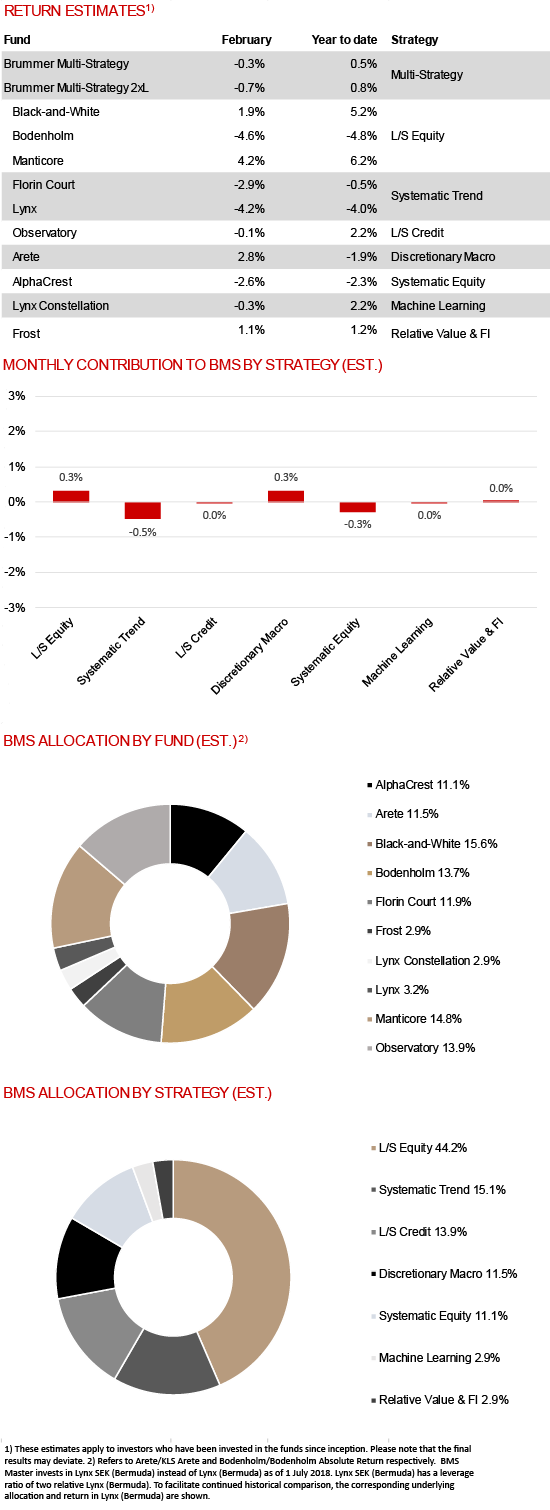

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated decline of -0.3 and -0.7 per cent respectively in February (-0.2 and -0.6 per cent for the corresponding USD classes).

MARKETS

Fears over the impact of the coronavirus caused a sharp sell-off across global stock markets towards the end of February. The yield on US 10-year treasuries fell to record lows as demand for safe havens spiked. In commodities, gold prices climbed to their highest levels since early 2013 before selling off at month-end, while the price of oil and gas fell on expectations of a decrease in global demand resulting from the coronavirus. It was also a volatile month for currencies with both the euro and Japanese yen rallying against the dollar during the last days of the month.

STRATEGIES WITHIN BRUMMER MULTI-STRATEGY

Long/short equity funds Manticore and Black-and-White both performed well in February with the former generating solid long alpha and the latter making money on stock specific gains, as well as on factor and sector hedges. Hong Kong based macro fund Arete also navigated the month well generating returns from relative equity positions. Relative value fixed income strategy Frost generated gains primarily from inflation trades. Long/short equity fund Bodenholm was the month’s largest detractor with losses primarily resulting from negative long alpha. Despite their beta neutral profile, systematic equity fund AlphaCrest also detracted. Trend following strategy Florin Court lost money on long credit positions, offsetting gains in power markets while trend follower Lynx lost money primarily on equity positions. Machine learning fund Lynx Constellation finished the month essentially flat, as did long/short credit fund Observatory.

As of March 1st, BMS’s portfolio managers only made some minor adjustments to the portfolio.