Brummer Multi-Strategy monthly commentary January 2020

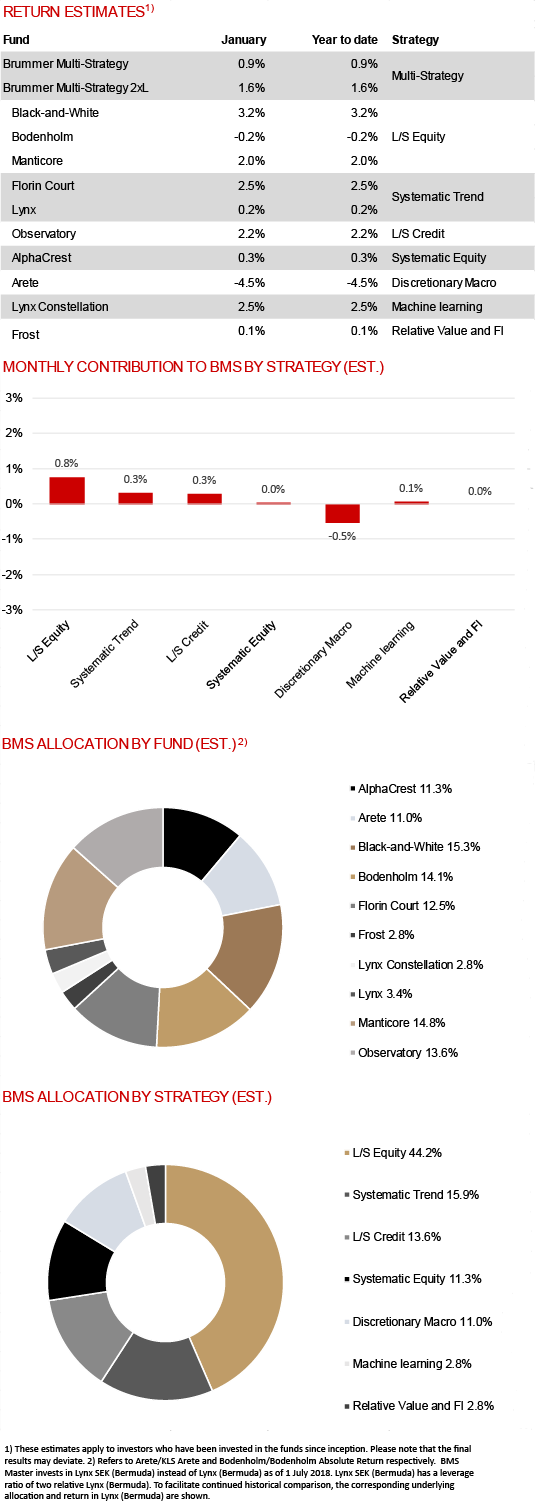

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted estimated returns of 0.9 and 1.6 per cent respectively in January (1.0 and 1.8 per cent for the corresponding USD classes).

Markets

January 2020 started with positive risk sentiment with US and China signing “phase one” of their trade agreement, calming hostilities between the two countries. US equity indices reached all-time highs despite slowing earnings growth and a soft industrial economy. The second half of the month however was dominated by concerns among investors about the spread of the coronavirus leading to a sell-off in global equity markets while oil prices fell on uncertainty regarding the virus’s effect on China’s economic growth. Gold and bonds, both safe haven assets, rallied and in currencies the US dollar strengthened while the Chinese yuan weakened.

Strategies within Brummer Multi-Strategy

January’s return was generated largely by positive alpha contribution from our long/short equity funds Manticore and Black-and-White. It was also a strong month for the long/short credit fund Observatory which made money on idiosyncratic credit positions and the trend following strategy Florin Court with profits in power markets being the main driver. Machine learning fund Lynx Constellation also had a good month, with gains primarily in commodities. Hong Kong based macro fund Arete had a difficult start to the year and struggled with the market turmoil following the coronavirus outbreak. The systematic equity fund AlphaCrest, fixed income relative value fund Frost, long/short equity fund Bodenholm and trend following fund Lynx were all essentially flat for the month.

As of February 1st, BMS’s portfolio managers only made some minor adjustments to the portfolio.