Brummer Multi-Strategy monthly commentary July 2020

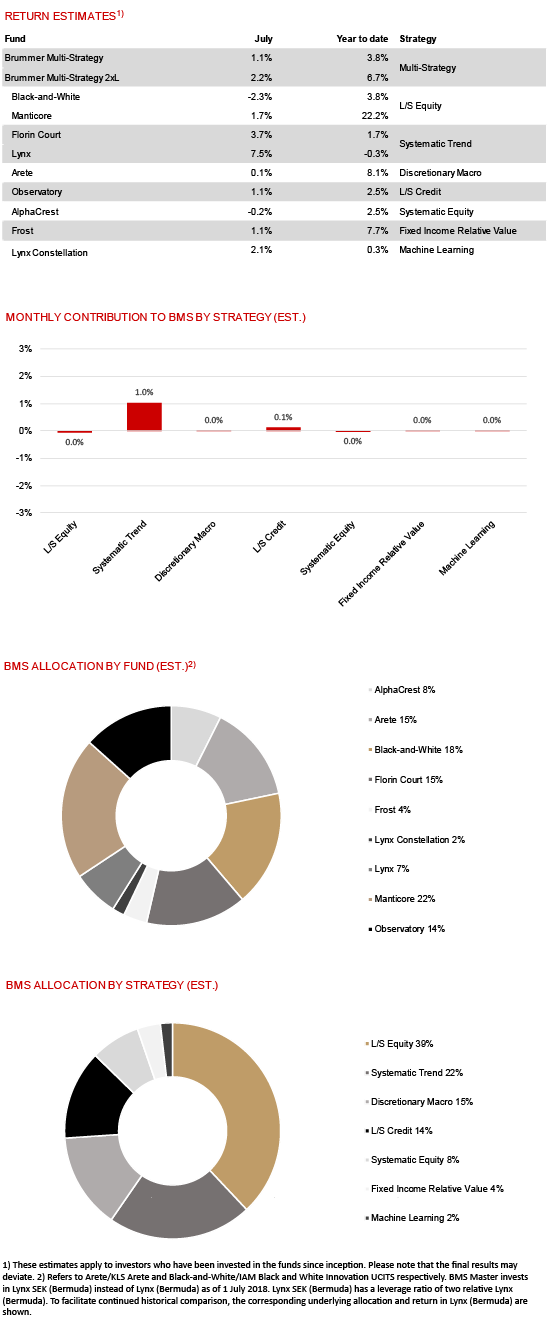

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted estimated returns of 1.1 and 2.2 per cent respectively in July (1.2 and 2.2 per cent for the corresponding USD classes).

MARKETS

Despite escalating US-China tensions and US and Euro area second quarter GDP falling by record numbers, equity markets rallied in July, fueled by coronavirus vaccine optimism and second quarter earnings generally surprising on the upside. In currencies, the US dollar weakened, primarily against other developed market currencies, while bond rates declined marginally. In commodities, the price of precious metals rallied while oil prices moved sideways during the month.

STRATEGIES WITHIN BRUMMER MULTI-STRATEGY

July was a good month for the trend following strategies Florin Court and Lynx as both made money across most asset classes. US based long/short equity strategy Manticore generated positive alpha during the month. Long/short credit strategy Observatory capitalised on various idiosyncratic relative value trades while fixed income relative value strategy Frost continued to profit from Scandinavian rates themes. Machine learning strategy Lynx Constellation also generated gains with equity indices trading being the main driver. Long/short equity strategy Black-and-White was the month’s only notable detractor mainly due to alpha specific losses. Hong Kong-based macro fund Arete and systematic equities strategy AlphaCrest both finished the month essentially flat.

As of August 1st, BMS’s portfolio managers only made minor adjustments to the portfolio.