Brummer Multi-Strategy monthly commentary June 2020

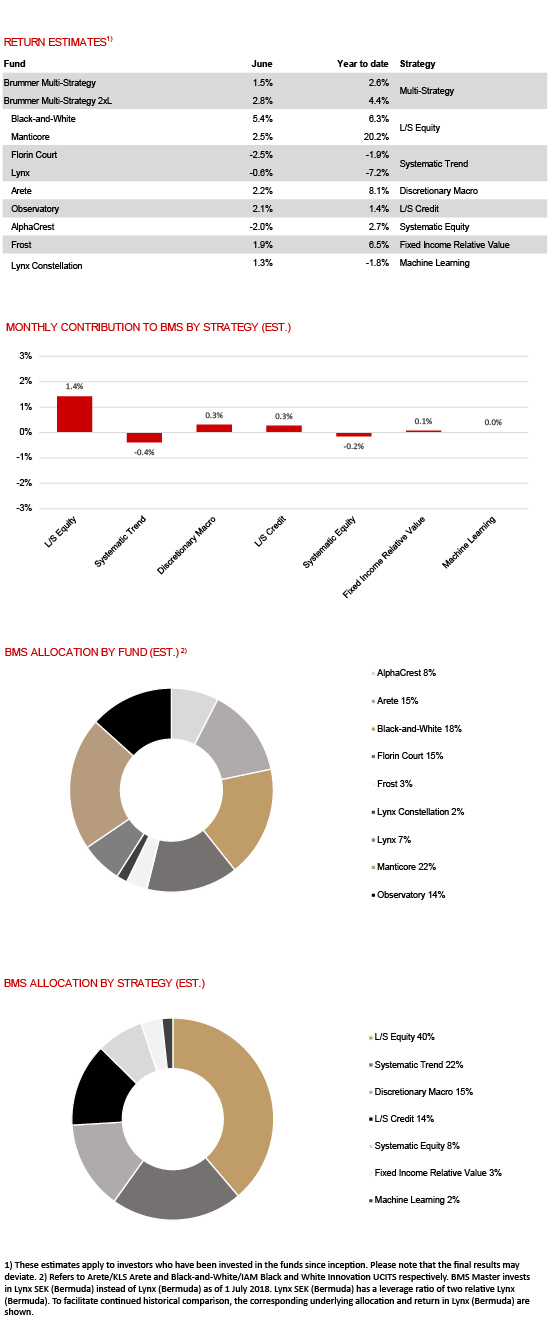

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted estimated returns of 1.5 and 2.8 per cent respectively in June (1.5 and 2.8 per cent for the corresponding USD classes).

Markets

Market volatility increased in June as hopes of improving economic activity and continued monetary and fiscal stimulus were weighed down by a resurgence in coronavirus cases in the US as well as an increase in geopolitical tensions. The price of gold rose to its highest level in almost eight years as investors sought safe havens while bond yields after briefly increasing at the start of the month remained at historic lows. In commodity markets oil prices continued their rally following supply cuts from both Russia and OPEC.

Strategies within Brummer Multi-Strategy

US based long/short equity funds Manticore and Black-and-White were the top contributors to BMS, with June proving an alpha-rich environment for both strategies. The Hong Kong based macro fund Arete also contributed positively capitalising on the rise in the price of gold as well as relative value equity positioning. It was also another strong month for L/S credit fund Observatory with idiosyncratic risk the main driver. Fixed income relative value strategy Frost and machine learning strategy Lynx Constellation also had strong months. Systematic trend follower Florin Court was the month’s largest detractor with positioning in power markets accounting for the majority of losses. Systematic equities fund AlphaCrest was down for the month while the systematic trend following strategy Lynx ended the month marginally in the red as gains in equities were offset by losses in foreign exchange positions.

As of July 1st, BMS’s portfolio managers only made minor adjustments to the portfolio.