Brummer Multi-Strategy monthly commentary September 2020

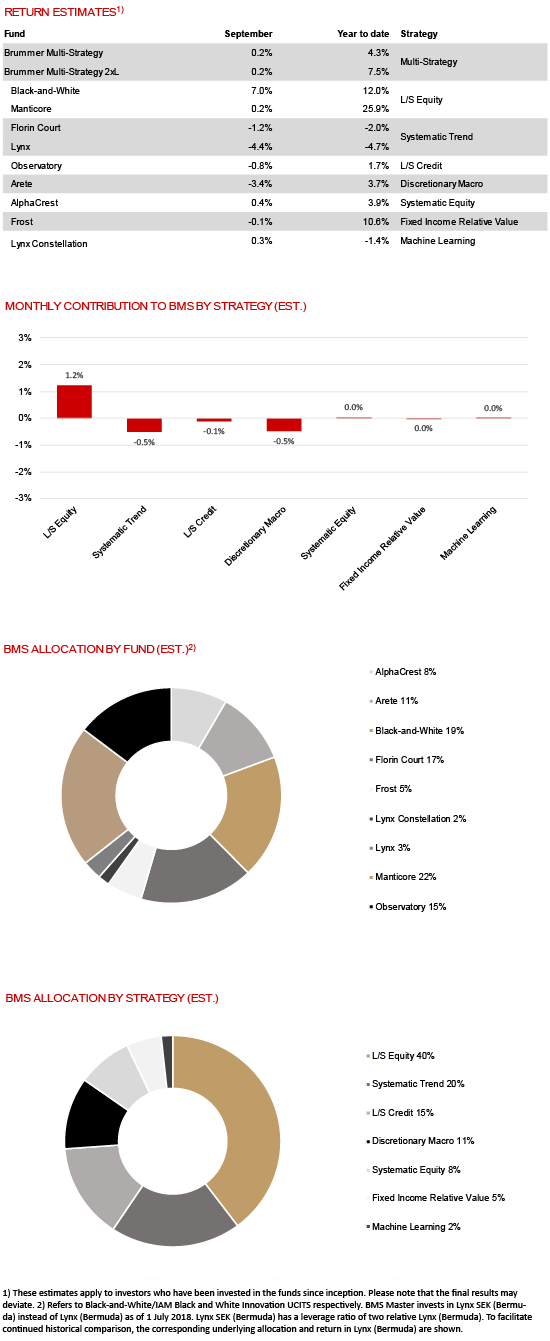

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted estimated returns of 0.2 and 0.2 per cent respectively in September (0.1 and 0.2 per cent for the corresponding USD classes).

MARKETS

September was a volatile month for equities with tech stocks leading the broader indices lower as markets priced in US election risk, new Covid-19 cases and an absence of new stimulus measures. The US dollar reversed its recent downtrend as risk sentiment slipped. In fixed income, US 10-year yield remained in the 0.65-0.70 per cent range despite market volatility. The price of precious metals fell while it was a choppy month for oil prices.

STRATEGIES WITHIN BRUMMER MULTI-STRATEGY

Another good month for long/short equity strategy Black-and-White with solid alpha generation, particularly from its long book. Systematic equities strategy AlphaCrest also managed to capitalise on the increase in volatility. The month’s main detractors were the macro strategy Arete and trend following strategy Lynx which both struggled being long equities, and short the US dollar for the latter. Long/short credit strategy Observatory was marginally down for the month, as was systematic trend following strategy Florin Court with gains mainly in fixed income and cash equities outweighed by losses in credit, power and FX positions. Fixed income relative value strategy Frost, long/short equity strategy Manticore and machine learning strategy Lynx Constellation were all essentially flat for the month.

As of October 1st, BMS’s portfolio managers decreased its allocation to Arete and Lynx with the proceeds distributed across the other strategies.