Brummer Multi-Strategy monthly commentary December 2023

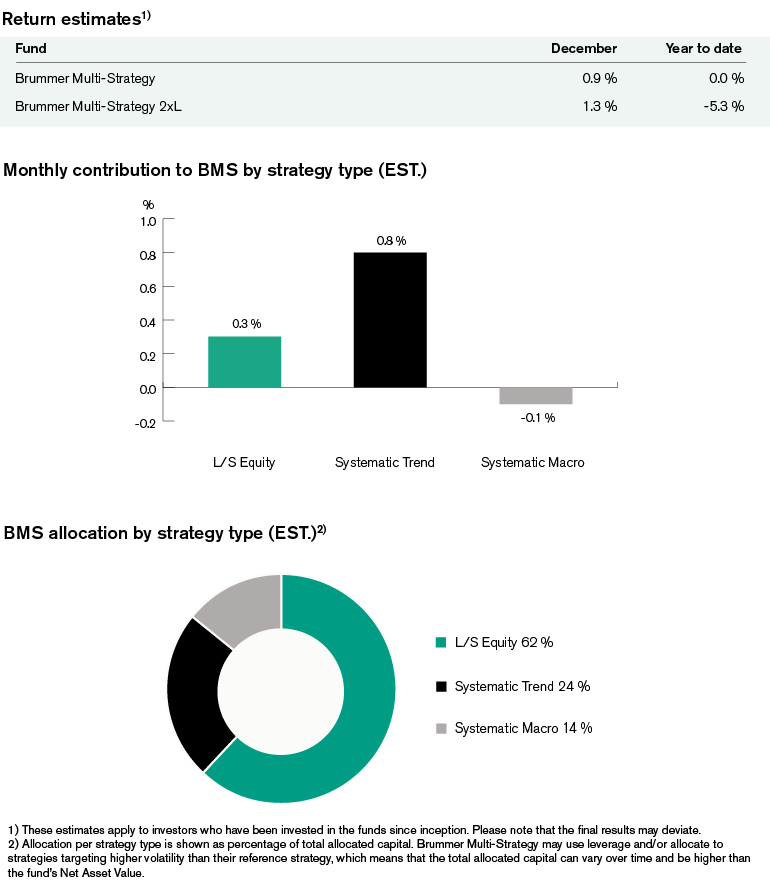

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated return of 0.9 and 1.3 per cent respectively in December (1.1 and 0.8 per cent for the USD classes).

Markets

December saw bonds and equities rally further on the back of various central banks, including the Fed, leaving rates unchanged and boosting market expectations of rate cuts in 2024. The ensuing climate proved fruitful in increasing the breadth of equity market returns to include a wider spectrum of companies as opposed to just a few market leaders . The shift in monetary policy narrative that began in November and continued in December helped drive treasury yields significantly lower and boosted the Nasdaq 100 to an all-time high. This, coupled with positive US macro data, with increased consumer spending, job openings and growth expectations for real wages, strengthened hopes for a soft landing for the U.S. economy. Market expectations that the Fed will cut rates at a faster pace than the rest of the world depreciated the U.S. dollar against a basket of currencies, in particular the Japanese yen and the euro. Oil prices oscillated during the month. Prices fell to a five-month low mid-month, even after OPEC+ constituents vowed to cut production, only to increase to approximately 80 USD/barrel following geopolitical tensions in the Red Sea. Meanwhile, gold fell initially, but ended the month slightly higher.

Brummer Multi-Strategy

Systematic trend-following posted a strong month in December, with gains coming from both developed and alternative markets. Trend-following proved particularly profitable in alternative markets, with significant gains from positions in power and credit. As for developed markets, positioning in fixed income and equities made money, while FX and commodities detracted somewhat.

Long/short equity ended up for the month. US TMT provided significant positive alpha. European financials contributed positively to the overall performance, with gains mainly attributable to the banking and diversified financials sectors. Positioning in the healthcare sector proved marginally positive thanks to profitable positions in healthcare equipment and pharmaceuticals. The main detractor for long/short equity this month proved to be the industrial sector, which was burdened by negative short alpha from positioning in capital goods which was partly offset by long alpha from the energy sector.

Systematic macro detracted marginally this month, with negative performance on developed markets partially offset by profits from alternative markets. For developed markets, the losses stemmed from equities, commodities and FX which were marginally offset by fixed income. As for alternative markets, the opposite was the case as gains from equities were offset by fixed income.

As of January 1st, BMS’ portfolio managers decreased the allocation to systematic trend-following somewhat and made some minor changes to the allocation within long/short equity.