Brummer Multi-Strategy monthly commentary August 2023

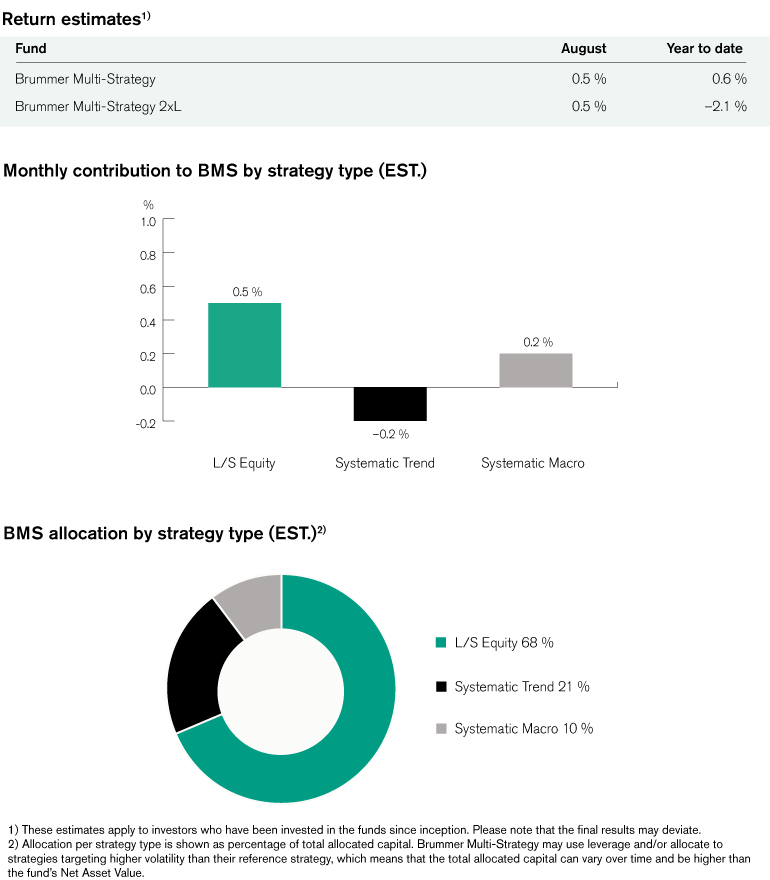

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated return of 0.5 and 0.5 per cent respectively in August (0.6 and 0.6 per cent for the corresponding USD classes).

Markets

Equity markets lost their momentum of positive returns in August, with the S&P500 and Nasdaq ending in negative territory. Strong US economic growth data, slowing core inflation numbers and a continued tight labour market has fuelled expectations of a goldilocks situation where the Federal Reserve may keep interest rates higher for longer. Real yields in the US surged during the month, with 10-year inflation linked bonds reaching their highest level since 2009. The US also announced an increase in its auction size of Treasury bonds which helped push yields higher. The rating institute Fitch downgraded the US long-term credit rating, highlighting, among other things, the country’s fiscal deficit. The Chinese economy continued to show signs of weakness with data for July showing falling consumer prices for the first time since 2021. In commodity markets, oil prices fluctuated following concerns about production disruptions, interest rate expectations and a stronger dollar.

Brummer Multi-Strategy

Systematic macro generated solid gains primarily in commodities and equities. Grains and metals were among the most profitable within the former mentioned asset class, and relative value positioning in US and Asian markets accounted for significant gains for the latter. Gains and losses were spread among currencies and rates on traditional and alternative markets resulting in more or less flat contribution in total from these asset classes.

Long/short equity had another strong month. Short alpha was the main driver of positive return across sectors this month for the strategy type. Positions in the European financials, fin-tech in particular, as well as Nordic/European TMT were fruitful. Names in the global industrials space contributed positively while US TMT positioning delivered moderate gains. Losses were realised within the global healthcare sector albeit finishing as a marginal detractor thanks to profits toward month-end.

Systematic trend-following detracted marginally for the month, with traditional markets finishing flat while alternative markets trading finishing the month negative. Gains in commodities contributed marginally positively but was offset by losses in equities, credits and currencies.

As of September 1st, BMS portfolio managers increased the allocation to systematic macro and marginally increased the allocation to long/short equity.