Brummer Multi-Strategy monthly commentary February 2024

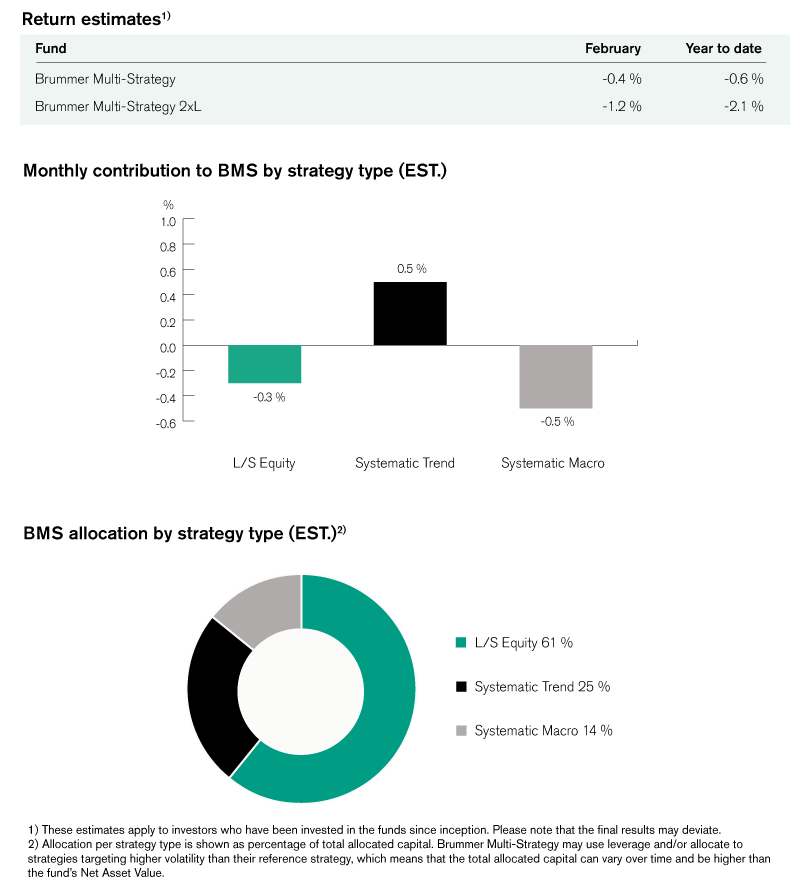

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated return of -0.4 and -1.2 per cent respectively in February (-0.3 and -1.1 per cent for the corresponding USD classes).

Markets

This February saw equity markets rallying to new heights, mostly driven by strong Q4 earnings reports delivered by large and mega cap names. Bolstered by tech names continuing to beat earnings expectations, the S&P 500 entered new territory by crossing the 5000 mark and dragging western markets with it. Eastwards the Nikkei 225 index reached a new all time high, a first since the Japanese bubble economy of 1989, mainly driven by names in chipmaking rallying towards the end of the month. On the other end of the spectrum, February saw sovereign bonds falling following a hawkish Federal Open Market Committee as well as a strong US CPI print shifting sentiment towards a postponement of rate cuts. In spite of the hawkish sentiment in US markets, February saw the US dollar depreciating slightly against a basket of currencies, with the yen holding steady in particular. Oil prices were volatile this month, due to a combination of tensions in the middle east, mixed economic data and a higher than expected US inventory, ultimately ending higher for the month. Elsewhere, gold ended flat while most other metals faltered.

Brummer Multi-Strategy

Systematic trend following proved to be the most profitable strategy for the month of February. In developed markets, profits were made in every asset class save for fixed income which detracted slightly. Positioning in alternative markets proved somewhat less profitable where gains in power and credit were to some extent offset by losses from fixed income and commodities.

Long/short equity strategies were a drag on performance this month. Profits can mainly be attributed to positioning in the US TMT sector, where hardware, consumer discretionary and semiconductors proved most profitable. European financials detracted this month, wherein negative short and long alpha from the banking and diversified financials theme was slightly offset by insurance gains. Positions in the healthcare sector was a small detractor for the month, where negative short alpha from healthcare equipment was slightly offset by long alpha from pharmaceuticals. The industrial sector ended roughly flat for the month, with profits from the energy sector offset by short positions in automobiles and capital goods.

Systematic macro was the main detractor this February, with losses stemming from positioning in alternative markets, commodities and equities in particular. On the other side of the spectrum, relative value strategies in developed markets proved profitable once again, as gains from commodities and bonds slightly offset the negative drag provided by positions in alternative markets.

As of March 1st, BMS’ portfolio managers allocated risk to a novel L/S equity strategy operating in the Consumer discretionary and TMT sector. In turn, the risk allocation to global industrials was decreased somewhat.

This is marketing communication. Please refer to the prospectus and to the KIID/KID of the relevant fund before making any final investment decisions.