Brummer Multi-Strategy monthly commentary June 2024

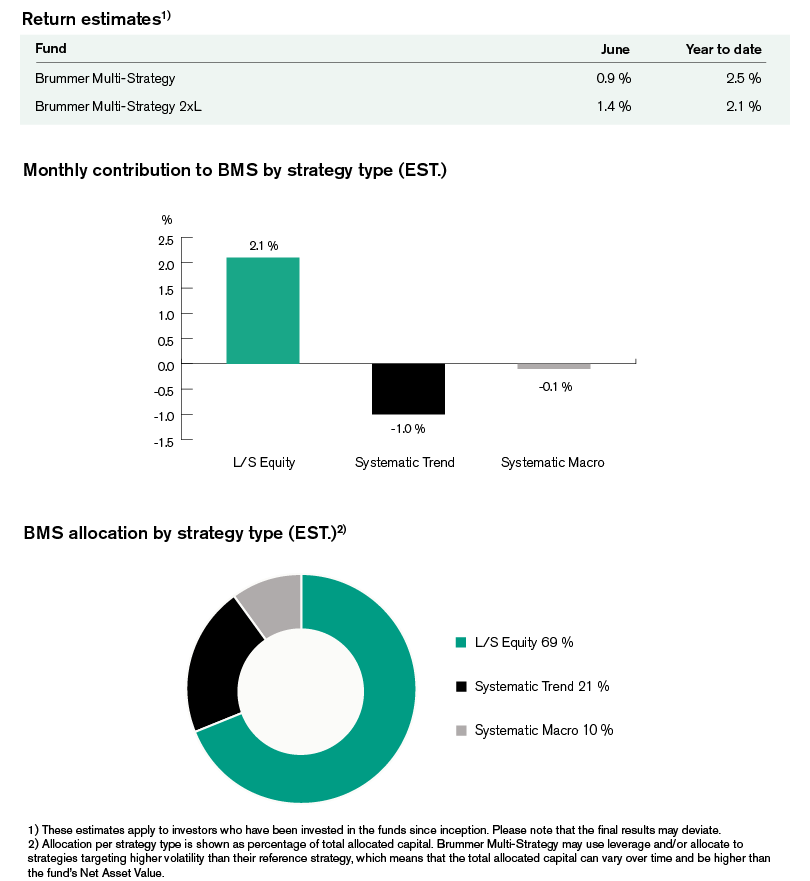

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated return of 0.9 and 1.4 per cent respectively in June (1.0 and 1.2 per cent for the corresponding USD classes).

Markets

This June, international politics and inflation once again took the spotlight as the two had opposing effects on markets to varying degrees. In the US, stocks in the S&P 500 saw a stable rally as a mix of CPI prints and unemployment figures signaled disinflationary pressure having effect. Across the pond, equity markets in Europe and UK faltered as political uncertainty over the two snap elections in France and the UK lowered investor confidence in their respective markets. The drops in performance for the FTSE 100 and STOXX 600 were slightly offset by the ECB cutting rates and inflationary figures coming in lower. In Japan, the Nikkei 225 rallied somewhat as weaker than expected inflation prevented further rate hikes. As a result of US inflation coming in lower than expected, US treasury yields moved lower with most of the Euro area yields also moving lower. The exception to this being France as political uncertainty put an upward pressure on the risk premia for French government bonds. On FX markets, the US Dollar appreciated somewhat against a wide basket of currencies on the back of strong economic activity in manufacturing and services. Most notably, the Japanese Yen slid to its lowest point against the dollar since October 1986, prompting the Japanese finance minister to publicly assure appropriate currency intervention. Elsewhere, oil prices saw a rather sharp rally following concerns about the Middle East combined with a rapidly declining US stockpile as well as geopolitical uncertainty brought on by the US presidential debate between Biden and Trump. In contrast, base metals such as aluminium, copper and nickel saw a rather sharp decline in June due to oversupply.

Brummer Multi-Strategy

In June, the trend following strategies faltered as short positioning in fixed income proved costly on both developed and alternative markets. Alternative commodity, fixed income, FX and credit markets were also detractors for the month. These losses were slightly offset by gains in equities.

Brummer Multi-Strategy’s long/short equity strategies proved to be the major performance contributor this month across the board. In the US TMT sector, solid performance was mostly attributable to positioning in the following sectors: semiconductors, software and services, as well as consumer discretionary; wherein solid alpha was realised within both the long and short book. Among European financials, gains in insurance were partially offset by losses in the banking sector. In global healthcare, gains were realised across all sub-sectors save for healthcare equipment.

This June, systematic macro strategies faltered somewhat with a marginal negative contribution overall. In developed markets, profitable positioning in FX and commodities was offset by losses in equities and fixed income. In alternative markets, losses stemming from positioning in commodities, FX and fixed income were in part offset by equities.

As of July 1st, Brummer Multi-Strategy’s portfolio managers decided to decrease the risk allocation to the systematic strategies operating in alternative markets, in favour of increasing the risk allocation to the systematic macro strategy operating in developed markets. Some adjustments were also made within the long/short equity bucket including the addition of a new long/short equity team operating in the healthcare sector.

This is marketing communication. Read the fund's information memorandum and key investor document (KID) before making any definitive investment decisions.