Brummer Multi-Strategy monthly commentary May 2024

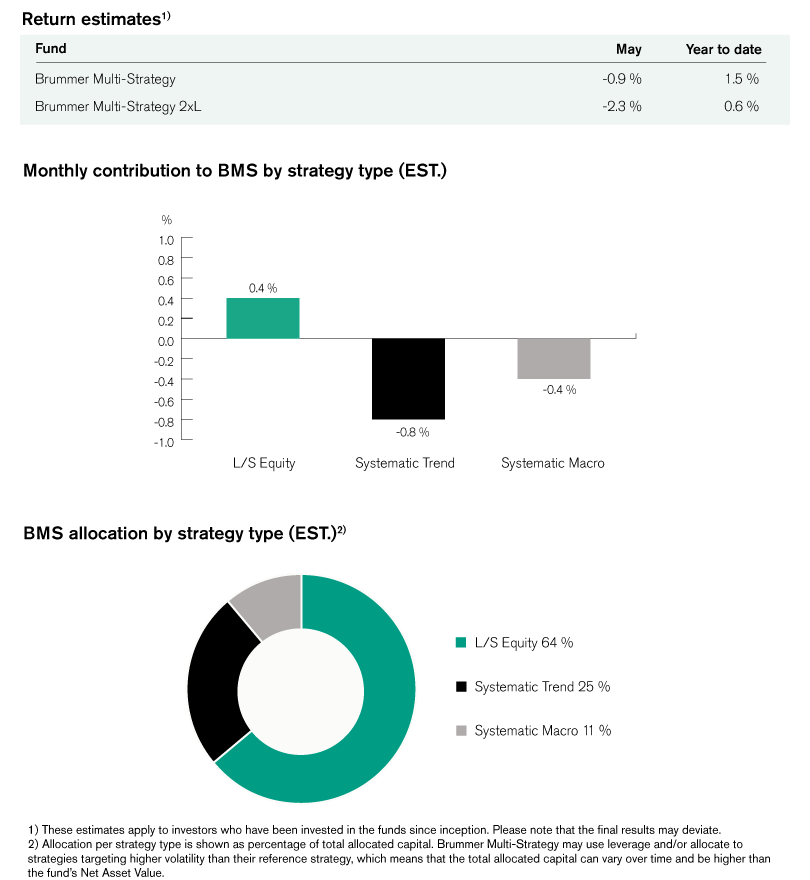

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated return of -0,9 and -2.3 per cent respectively in May (-0.8 and -2.1 per cent for the corresponding USD classes).

Markets

In May, US equities proved to be a solid standout in an otherwise turbulent investing climate. A mix of sound macroeconomic data, signs of cooling inflation as well as strong Q1 earnings reports from key names drove the S&P 500 to new highs. On the other side of the Atlantic, the STOXX 600 and FTSE 100 started out with solid performance which tapered off towards the end of the month as improved economic activity and thus higher inflation rates lowered rate cut expectations. In Japan, the Nikkei 225’s performance was hampered for the month, ultimately ending flat as higher rates and disinflationary worries put negative pressure on Japanese industries, worsened by a record-weak yen. With the FOMC announcing no change in interest rates and other signs of cooling US inflation, Treasury yields moved lower in May from their April 2024 peaks. This contrasted with UK Gilts and German Bunds, whose yields moved higher on the back of strong economic data and a high CPI print. The change in investors’ sentiment concerning rates led to the US dollar depreciating against the pound and euro, with the only major currency to depreciate against the dollar proving to be the yen which as previously mentioned ended in record low territory. Meanwhile, hopes of a potential ceasefire in tandem with a US oil inventory increase moved Brent crude and WTI Oil prices lower for the month while silver and platinum prices rose significantly.

Brummer Multi-Strategy

The biggest detractor for BMS proved to be the trend following strategies in May. In developed markets, losses stemming from FX and commodities proved too great to be weighed up by gains in equities. Positioning in alternative markets also proved less than fruitful as modest gains in credit and equities were outweighed by losses in commodities, fixed income and FX.

Long/short equity contributed with strong performance this month. The US TMT sector saw solid alpha gains with profitable short positions in software & services and long positions in media & entertainment being slightly offset by positioning in tech hardware and semiconductors. One particularly profitable sector this month proved to be European financials, where gains were realised across all sub-sectors; banking, diversified financials and insurance. Positioning in global healthcare proved less profitable this month, with negative alpha mainly attributable to losses in pharmaceutical names which were partially offset by gains in life sciences.

Systematic macro contributed negatively to BMS performance. In developed markets, gains in equities were offset by losses in commodities and fixed income. In alternative markets, losses were realised across sectors with FX detracting the most.

As of June 1st, BMS’s portfolio managers decided to rebalance the risk allocation between the two systematic macro strategies, with the allocation to alternative markets decreasing in favour of the strategy on developed markets. The risk allocation to the L/S equity strategy within the US TMT sectors was also increased somewhat.