Brummer Multi-Strategy monthly commentary September 2024

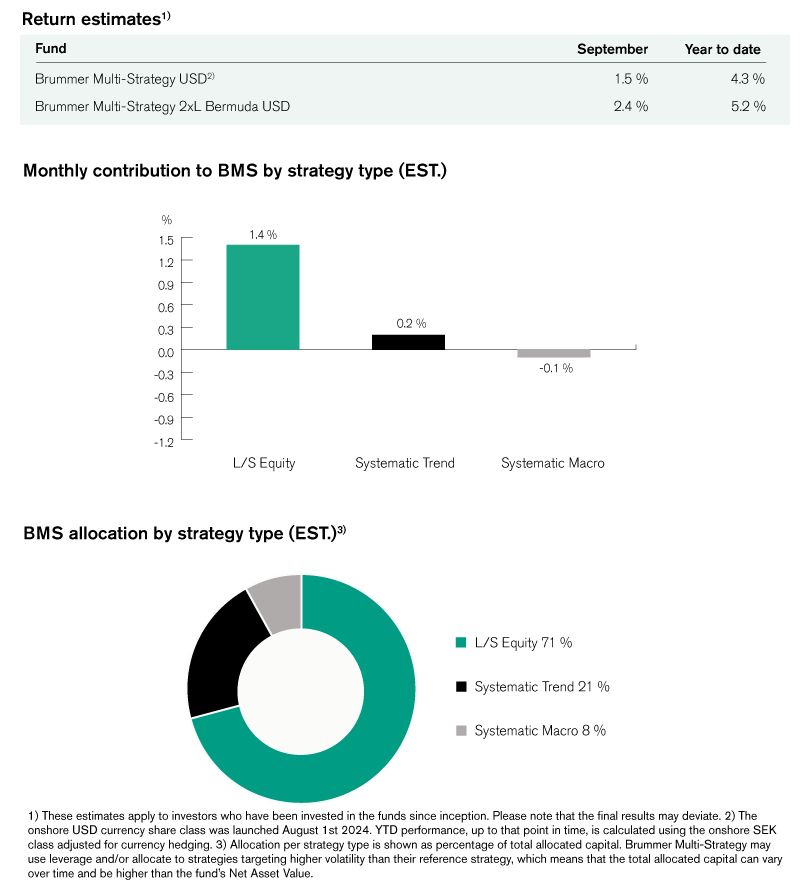

Brummer Multi-Strategy (BMS) USD and Brummer Multi-Strategy 2xL (Bermuda) USD posted an estimated return of 1.5 and 2.4 per cent respectively in September.

Markets

The month of September saw a continuation of the rally in risky assets as monetary and fiscal intervention swept across the globe. In equities, western markets initially tumbled on the back of US recession fears brought on by slightly weaker than expected US labour market data. This proved short-lived however, as indices quickly rebounded in tandem with ECB’s rate cut, as well as in anticipation of the Fed announcing their rate cut. The steeper than expected cut of 50 basis points saw US equity markets rally as the cut signalled the beginning of the end of the high interest rate regime. Ultimately, equity markets in the west ended the month on a positive note, with the exception of the UK stock market. In Japan, the Nikkei 225 ended flat for the month after the appointment of Shigeru Ishiba as the next prime minister sent domestic stock indices lower due to fears of potentially market-unfriendly policies. In China, the PBOC and Politburo unveiled plans for the country’s largest stimulus package since the pandemic (consisting of rate cuts and lowered reserve requirement ratios for banks) causing the Hang Seng and Shanghai composite indices to skyrocket into double-digit territory in a matter of days.

As central banks eased their respective policies, sovereign bond yields moved lower overall but to differing degrees. In Europe, yields moved lower on the back of ECB’s rate cut as well as the Eurozone inflation falling below expectations indicating a higher magnitude of rate cuts in the following months. In the US however, bond yields initially slid lower but rebounded slightly after the announced rate cut due to signalling from Fed chair Jerome Powell that they would opt for smaller cuts in upcoming meetings. In FX markets, the US dollar depreciated against a wide basket of currencies, with the yen strengthening in particular due to Ishiba’s indication of tighter monetary policy under his regime. Following Saudi Aramco pledging to increase their oil production and warring factions in Libya agreeing on a central bank chairman (which could suggest a restart of the domestic oil production), oil prices moved lower for the month while metals, precious and base, moved higher due to easing of monetary policy as well as expectations of increased industrial production now that China has a stimulus package to look forward to.

Brummer Multi-Strategy

BMS’s systematic trend following strategies contributed positively to the overall performance of the fund. In developed markets, profitable positioning in fixed income, equity indices and FX were partially offset by losses stemming from commodities. Contribution from alternative markets were flat when profits in fixed income, credit and FX were offset by losses in commodities and power.

While the various sectors within the long/short equity bucket diverged from one another, they provided the overall greatest contribution to performance this month. Within the US TMT sector, gains were realised across all sub-sectors save for capital goods and semiconductors, with gains materialising primarily in the long book. Positioning in global healthcare sectors were less fruitful as gains in healthcare equipment were offset by long positioning in pharmaceuticals and life sciences. In European financials, solid alpha was generated within the banking and insurance sector in both the long and short book. In particular, the Nordic and Continental banking themes contributed alpha, while diversified financials detracted some.

The systematic macro bucket ended roughly flat for the month, with the common denominator being gains in fixed income and FX offset by losses in commodities and equities.

As of October 1st, BMS’s portfolio managers decided to rebalance the risk within the long/short equity bucket somewhat.

For more information on Brummer Multi-Strategy's performance, please see the tables and graphs below.

This is marketing communication. Read the fund's information memorandum and key investor document (KID) before making any definitive investment decisions.