Brummer Multi-Strategy UCITS monthly commentary January 2024

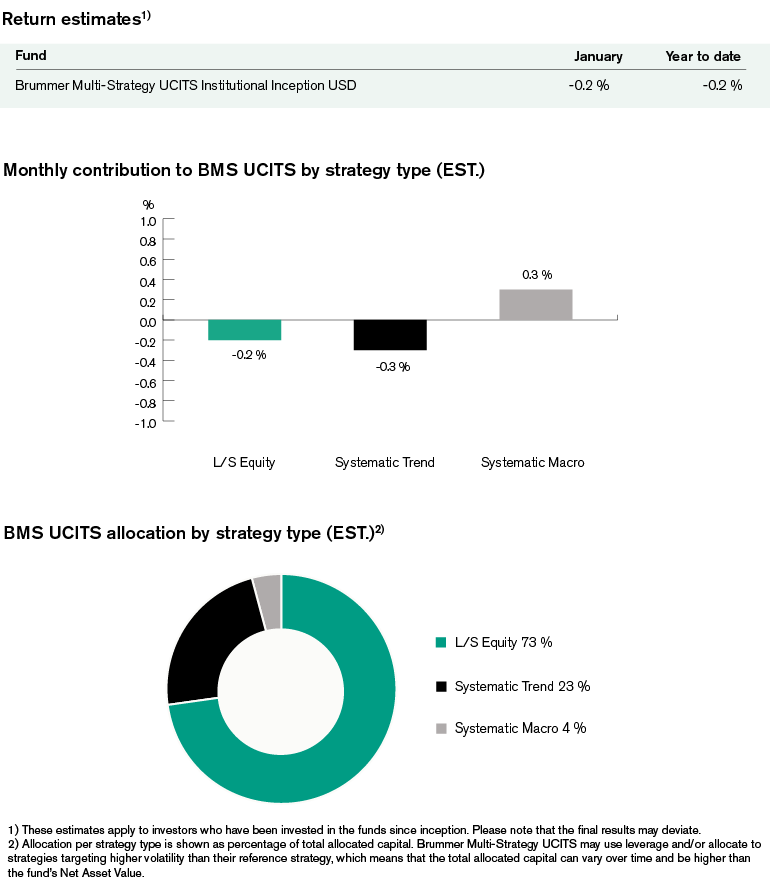

Brummer Multi-Strategy UCITS (Inst. Inception Class USD) posted an estimated return of -0.2 per cent in January.

Markets

Equities proved to be a mixed bag in January as large and small caps moved in opposite directions. While mega-cap tech names helped the S&P 500 recover from a rocky start to hit all-time highs on the back of strong PMI and consumer prints, the Russell 2000 meanwhile continued lower. Similarly in Europe, following the ECB leaving rates unchanged and the German PMI proving strong, the Eurostoxx 50 ended on a positive note while the FTSE Europe Small Cap index ended down. Eastwards, the Nikkei 225 continued to climb closer to its 1989 all-time high on the back of lower inflation and unchanged rates from the BoJ while the Hang Seng index continued its downward spiral fuelled by mainland China’s bleak economic outlook as well as the ordered liquidation of the Hong Kong-listed real estate giant Evergrande. January saw yields rising in anticipation of inflation data and policy announcements from central banks. US yields rose somewhat, rising marginally in spite of lower-than-expected core PCE data, only to fall thereafter ending the month relatively flat. The same could be seen in the Eurozone, as the German Bund yield rose steadily only to taper off at the end of the month. The US Dollar appreciated throughout the month against a wide basket of currencies on the back of a repricing of rate expectations in the US. The month ended with a somewhat hawkish Federal Reserve and risk-off market sentiment. Continued hostilities in the Red Sea in tandem with dwindling US supplies drove oil prices to their highest level since November 2023. Meanwhile, gold held fast while other precious metals faltered.

Brummer Multi-Strategy UCITS

Trend following detracted somewhat during the month primarily due to losses in alternative markets, namely short dollar vs emerging market currencies and long bonds in emerging markets the main drivers. Developed market trend following, however, had good month capitalising on trends in equity markets in Japan and Hong Kong.

Market neutral long/short equity was a small negative drag on performance in January. Gains were generated primarily in the US TMT sector with positioning in software as well as media and entertainment names performing well. European financials also had a good month with solid alpha contribution primarily from various bank themes. Positioning in the healthcare sector finished roughly flat for the month with solid short alpha in the pharmaceuticals space. The primary detractor in January was positioning in the industrials sector with long names in materials and capital goods proving costly.

Systematic macro was the best performer in January, where relative value positioning proved particularly fruitful in Asian equities given the performance spread between Japan and Hong Kong. FX was also solidly profitable.

As of February 1st, BMS UCITS portfolio managers decreased the risk allocation to the industrial sector within long/short equity.

This is marketing communication. Please refer to the prospectus and to the KIID/KID of the relevant fund before making any final investment decisions.