Brummer Multi-Strategy UCITS monthly commentary October 2024

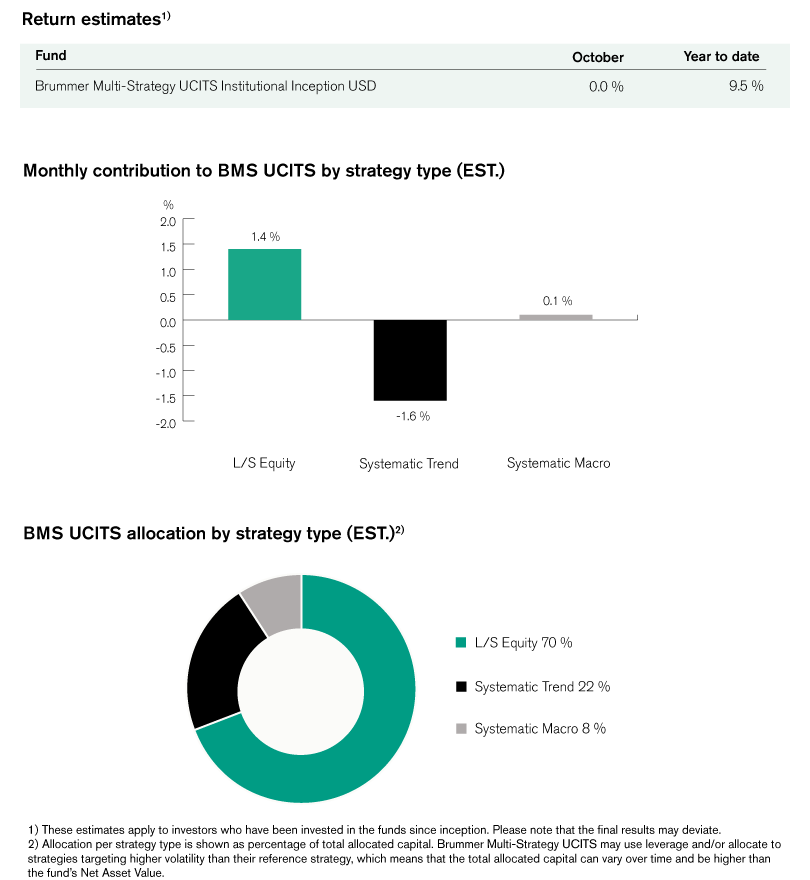

Brummer Multi-Strategy UCITS (Inst. Inception Class USD) posted an estimated return of 0.0 per cent in October bringing year to date performance to an estimated 9.5 per cent.

Markets

October proved to be challenging month for markets with both bonds and equities declining. In the US, equities saw a slight upward trend hampered by higher bond yields as markets anticipate less aggressive rate cuts from the Fed in the coming months due to a stronger than expected US workforce as well as a potential Donald Trump victory. European equities saw similar a development throughout the month, with all major western indices ultimately ending in the negative with a rather large drop month-end, potentially due to investors selling off ahead of election day on November 5th. In Japan the Nikkei 225 index oscillated following hawkish signals from the BoJ as well as weak economic data. China however, saw a dramatic price drop on its indices as the central government offered no clear indication of any additional stimulus packages. In fixed income markets, sovereign bond yields moved higher overall in the west as strong economic prints helped keep inflation elevated. In the US, bond yields rose in anticipation of another Donald Trump presidency bringing expectations of more protectionist trade policies. Fears of more US tariffs under a Trump regime brought with it a stronger US dollar, which gained against most major currencies. In commodity markets, it was a volatile month for oil prices as tensions between Israel and Iran tugged on prices. Prices initially spiked as markets anticipated an Israeli counterattack on Iranian oil reserves, only to drop when it did not transpire. Elsewhere, gold continued to appreciate to record levels while silver also had a strong month.

Brummer Multi-Strategy UCITS

In October, BMS UCITS’s market neutral long/short equity teams generated solid positive contribution to performance. In the US TMT sector, strong alpha within the semiconductor and software spaces was slightly offset by long positioning in consumer durables as well as commercial and professional services. In global healthcare, profitable short positioning in healthcare equipment and biotech was offset by less than favorable positioning in life sciences and consumer health sectors. Positioning in European financials detracted this month, mainly led by negative alpha from banking in the Nordic and Italian regions as well as some Asia-exposed insurers. This was partly offset by positive performance within the Continental European banking theme as well as some reinsurance and composite insurance names.

The systematic macro bucket ended marginally positive for the month, mainly driven by relative value positioning on developed markets. There, performance was positive in all asset classes save for fixed income. On alternative markets, profitable positioning in commodities was entirely offset by losses in FX and equities.

The main detractor to performance this month was the systematic trend bucket, both on developed and alternative markets. In the case of the former, the main detractors proved to be positioning in fixed income and FX markets. The same could be seen on alternative markets, where FX and fixed income detracted and were somewhat offset by gains in commodities.

As of November 1st, BMS UCITS’s portfolio managers decided not to make any significant changes in the risk allocation in the portfolio.

This is marketing communication. Read the fund's information memorandum and key investor document (KID) before making any definitive investment decisions.