Brummer Multi-Strategy monthly commentary May 2025

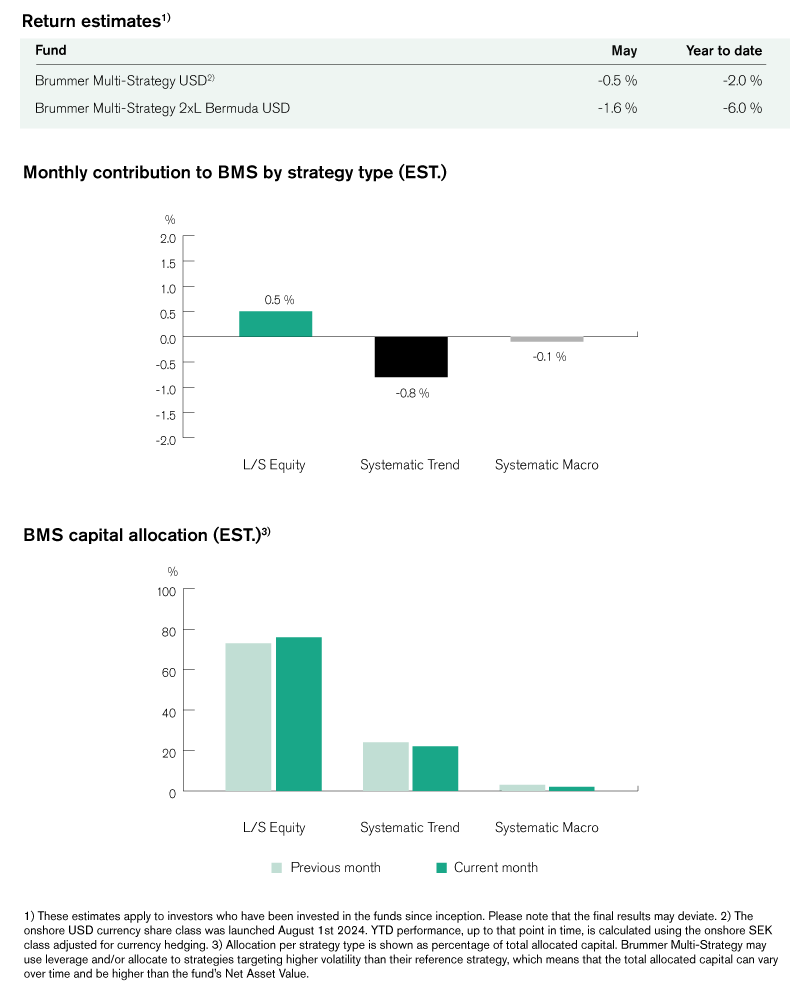

Brummer Multi-Strategy (BMS) USD and Brummer Multi-Strategy 2xL (Bermuda) USD posted estimated returns of -0.5 and -1.6 per cent respectively in May.

Markets

Markets staged a sharp rebound in May, with U.S. equities delivering their strongest monthly performance since late 2023. The S&P 500 climbed +6.2% bringing it into positive territory for the year while the Nasdaq finished +9.6% for the month. Risk appetite returned in force as investors took comfort in a notable de-escalation of trade tensions. The month’s turning point came as Donald Trump backed away from some of his most severe tariff threats, easing concerns over a renewed global trade conflict. A temporary 90-day tariff truce between the U.S. and China, along with the announcement of a U.S.-UK trade deal, buoyed sentiment.

Despite the surge in equities, concerns around U.S. fiscal health came back into focus. Moody’s downgraded the U.S. credit rating, while Trump’s proposed “big, beautiful” tax bill raised fresh questions about the sustainability of rising deficits. U.S. 10-year Treasury yields climbed 24 basis points to 4.4%, reflecting heightened concerns over long-term debt dynamics.

Meanwhile, the U.S. dollar finished the month marginally negative against a basket of major currencies. The divergence between rising yields and a weakening dollar underscores the growing investor unease with U.S. fiscal policy, even as risk assets rallied.

In commodity markets, crude oil initially rallied but stalled following the surprise decision by Opec+ to increase production.

Brummer Multi-Strategy

May was another difficult month for systematic trend following with the biggest losses attributable to fixed income, where long bond positioning in the short end of the curve was costly (mainly US). In FX, losses in JPY/USD and CNH/USD positioning outstripped gains in GBP/USD. In commodities losses came primarily from short Brent Crude Oil and long coffee positioning. Some gains came from equity futures and to a lesser degree from credit. Given the relative high volatility and trend sparse environment, our trend following teams have cut risk across the board and have very reactive portfolios (e.g. in the event of a paradigm shift, they will quickly be able to position for new trends).

Within market neutral long/short equity, positive alpha was generated across most sectors in May, with gains primarily stemming from positioning in listed real estate, consumer discretionary and U.S. TMT. Our L/S equity teams have started to increase their gross exposure during the month, reflecting greater conviction and a richer opportunity set.

Systematic macro saw losses mainly in fixed income positioning in May with positioning in the Australian long end of the curve and the U.S. short end the main losers.

This is marketing communication. Read the fund's information memorandum and key investor document (KID) before making any definitive investment decisions.