Monthly commentary BMS June 2017

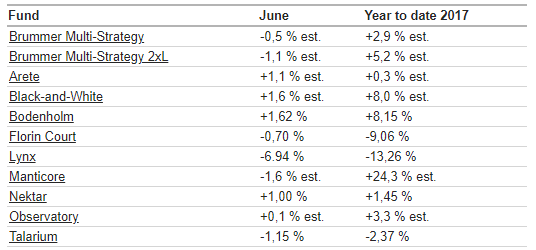

Brummer Multi-Strategy (BMS) returned -0.5% in June which brings performance year to date to 2.9%. Hedge Fund Research’s fund-of-fund index posted a decline of -0.6% during the month bringing its performance during 2017 to 2.6%.

In June the Federal Reserve raised interest rates. Equity markets saw sector rotations with tech shares, which had performed strongly during the beginning of the year, weakening whereas financials and other laggards gained. The US Dollar declined against the Euro and British Pound. Oil extended sharp declines.

Among the funds that BMS invests in, the top contributors for the month were the long/short equity funds Black-and-White and Bodenholm which both has generated a strong positive alpha, meaning return that is independent of the performance of the market. June was however a difficult month for the trend following fund Lynx with one of the strategy’s worst months since inception. The fund was positioned for increasing equity prices, lower bond yields and commodity prices, and a stronger US dollar. The losses were mainly generated during the second half of the month, when markets moved against almost all of these positions.

BMS’s net exposure towards equities and commodities ranged between +30 and +25 percent and closed out the month at around +25 percent. The portfolio allocation to Black-and-White, Bodenholm, Nektar and Observatory increased while Manticore and Arete received a reduction in their weighting.