Monthly commentary BMS November 2018

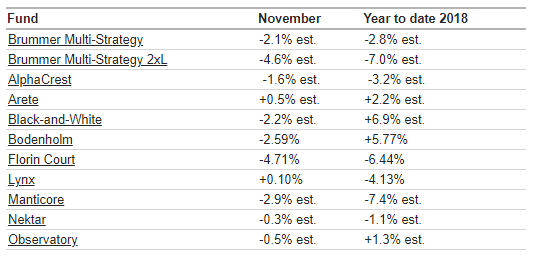

Brummer Multi-Strategy (BMS) SEK delivered an estimated return of -2.1 percent for November. The YTD estimated return now amounts to -2.8 percent . The corresponding figures for the USD class amounts to -1.9 percent and -0.4 percent respectively.

The main reason for our continued losses in November is alpha rather than beta (market exposure). The market exposure, defined as the net equity exposure, and equity beta, both hovered around low single digits during the month. The forces of deleveraging continued, which proved a challenging market environment for our L/S equity funds which continue to struggle with vast and erratic price movements. As we wrote in our October note, some explanatory factors driving market movements rather than stock specific fundamentals are continuing de-risk and deleveraging forces – as speculative investors in general continue to decrease leverage and risk, causing fierce spillover effects and spirals of prices going both up and down. According to prime brokers the de-leveraging process in equites during October-November is the most severe since they started counting ten years ago. The average monthly loss for our L/S equity funds stood at -2.3 percent. Furthermore, choppy markets and erratic price movements made it difficult for the exotic CTA fund Florin Court which ended down 4.8 percent. The main losing asset classes for Florin Court in November was commodities, emerging markets fixed income and currencies. Lynx, on the other hand, managed to deliver a marginal positive return.

Our macro-oriented funds Arete, Nektar and Observatory have in general coped better than our other strategies in October and November, generating slightly positive returns in total.

The nervousness and overall stress levels in the market are indeed very high as investors react to news about geopolitical challenges, such as trade wars, and incoming economic data which continues to indicate a slowdown in global growth. In general, hedge funds have not been able to offer much protection, e.g. the global hedge fund index HFRX is now down 5.2 percent YTD in USD terms.

Going into December, BMS changed the allocation in the portfolio to take a more defensive stance. Hence, the allocation to L/S equity funds was decreased significantly and the allocation to our macro funds and CTAs increased. In our October note, we also commented on the medium to long term outlook and the probability of an equity bear market. Incoming data are indeed confirming a slowdown in global growth and the probability for a downward trend for risky assets appears to have increased. As we also stated, we believe that BMS over the medium to long term is in a good position to meet our investment objectives. Adapting to a likely new market regime will probably be painful for a lot of investors, but we believe our hedge fund mandate provide us with the necessary tools to adapt and deliver absolute returns. In times of short term stress, one should plan for the longer term and from that perspective we remain confident.