Monthly commentary BMS October 2018

Brummer Multi-Strategy (BMS) declined -4.0 percent and -3.0% (SEK and USD class respectively) in October. The respective YTD returns are -0.8% and +1.5%.

October marked another severe sell-off for financial markets. Most equity markets are now in negative territory YTD and in Europe between -3% to -12%. Bond markets have not offered much protection. It has also been a tough year for hedge funds in general – as of October 29th, the main global hedge fund index HFRX was down 5% YTD (USD class).

Performance

• A significant part of our October loss was stock specific (alpha) rather than due to the overall market exposure (beta).

• Our objective is to limit BMS’s loss to 3% in a month or 5% in a quarter. Risk management is a mix of art and science and sometimes we and our fund managers get it wrong.

• BMS is now well positioned to protect against further market sell-offs.

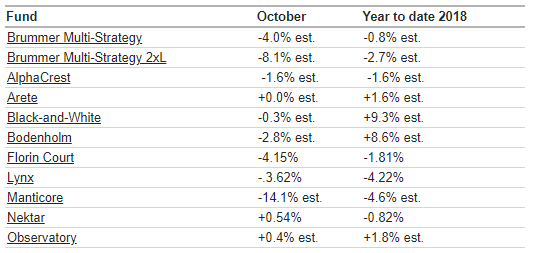

BMS was down approximately 4% for the month. Manticore generated the largest negative contribution to BMS, -2.4%. Our trend-following strategies accounted collectively for -1.1% of BMS’s loss while two of our other equity funds, Bodenholm and AlphaCrest, also had a challenging month. Only Nektar, Observatory and Arete posted positive performance for the month. Black and White was marginally down.

Within Long-Short equity, roughly half of the loss was driven by market exposure and half by stock selection. The vast majority of poor stock performance is the result of a poor earnings season. In addition to a poor hit ratio, losses have escalated due to a deleveraging process by speculative investors, causing for example popular short positions to rally when market participants are forced to de-risk their portfolios. Indeed, it has been a tough environment to navigate for stock pickers, and our funds were no exception.

Our trend-following (CTA) funds also suffered in October, costing BMS a quarter of the monthly loss. Both our CTAs had long equity exposure at the beginning of the month which contributed to their losses, but the majority of the losses were caused by sharp reversals in commodities such as power, oil, gold, and silver. Parts of these trend reversals can also be explained by forced deleveraging which occurs when CTAs and similar strategies adjust their positions due to increased volatility and price reversals. The quicker the corrections, the more difficult for these strategies.

On the positive side, both Nektar and Arete have been able to generate some profits in both the bond and currency markets. Observatory profited from relative value credit positions.

From a strategic allocation perspective, BMS has been overweight Long-Short equity strategies and underweight CTA strategies. We recently addressed this theme by marginally reducing the allocation to Long-Short equity and increasing that to CTAs. BMS has also had relatively high allocations to both Nektar and Observatory primarily for diversification reasons. Unfortunately, given the absolute levels of losses and gains, our portfolio construction theme did not contribute much in October, partly because some of the anticipated defensive exposures did not offset other losses. Exposure to the increased implied volatility in rates, a stronger USD, and steeper curves were some of these positions.

Where do we go from here?

Is this another example of a severe correction or are we entering a bear market after a 10-year bull market? We do not know yet. What we do know is that it is easy to be bearish. Compared to the significant correction in February this year, several themes have evolved, the most prominent being increased interest rates due to central bank tightening, which in turn impacts equity valuations. Recent signs of slowing growth in Europe and China, as well as heightened geopolitical risk, have potential implications clearly for the global growth prognosis, but also for corporate earnings. In addition, financial market sentiment has recently shifted, demonstrated most clearly by the stronger market reaction to modest or weak reports versus the comparatively subdued response to solid earnings reports and positive future earnings potential. Furthermore, the room for further fiscal and monetary stimulus appears limited.

On the other hand, US growth is still strong and trade wars and other issues might be resolved. Incoming economic data and corporate activity will be very important to monitor in the short term.

From a BMS perspective, despite the recent month, we remain confident that we are well positioned to deliver returns during a bear market scenario. Despite recent losses in our Long-Short equity funds, we are confident they will be able to perform on both long and short positions, given signs of increasing dispersion across sectors, some of which are entering downcycles. Our CTAs are now flat or short equities across their books and hence prepared for a bear market. In general, an environment with increased volatility and focus on fundamental data is good news for our macro funds.

The most challenging scenario for us short term is probably a swift market rebound followed by a range bound market trend. Such an environment does not necessarily mean we will underperform, but overall it is not an ideal environment for either the fundamental or systematic strategies within BMS.

Once again, we are disappointed with recent performance. Despite a strong focus on portfolio construction and managing market exposure the losses were larger than expected due to poor alpha. Over the medium- to long-term we however remain confident that BMS is strongly positioned to meet our investment objectives.

Finally, we would like to thank you for your trust and support.

Best regards,

Patrik Brummer and Mikael Spångberg

Brummer Multi-Strategy Portfolio Managers