Brummer Multi-Strategy monthly commentary September 2021

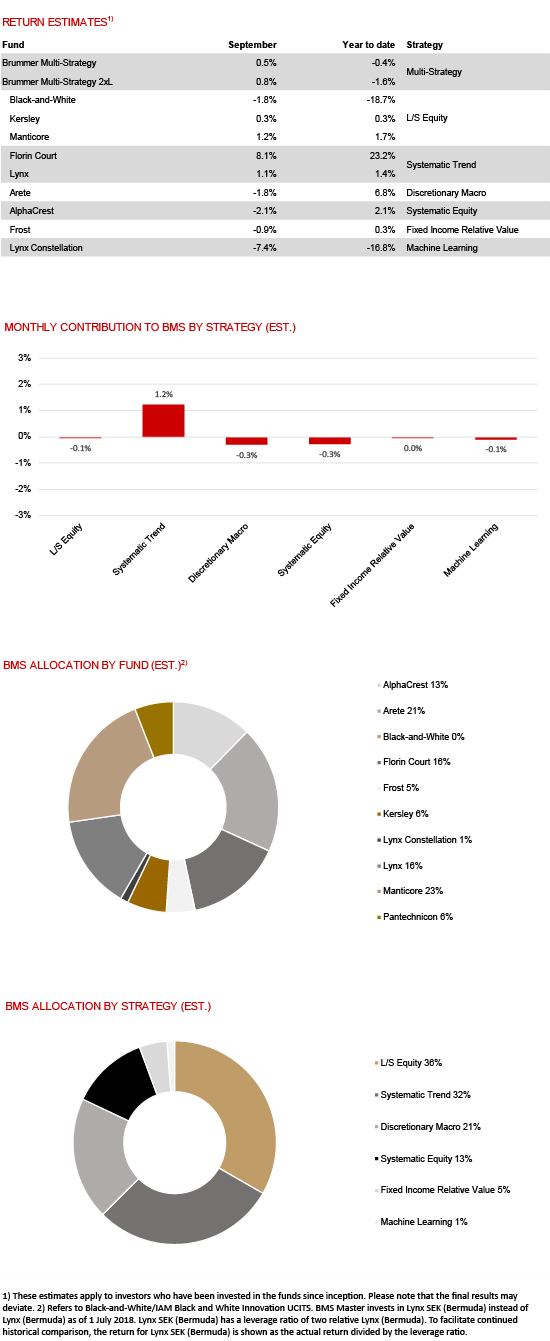

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated return of 0.5 and 0.8 per cent respectively in September (0.4 and 0.9 per cent for the corresponding USD classes).

Brummer Multi-Strategy AB announces new leadership, starting in October, with Markus Wiklund as Managing Director and Kerim Celebi as Portfolio Manager for BMS together with Patrik Brummer. The team is further strengthened by the addition of a new Risk Manager in Andreas Ekenbäck. Mikael Spångberg leaves the firm due to private reasons. Click here to read more.

MARKETS

September began with the S&P500 and Nasdaq reaching new all-time highs. However, sentiment shifted quickly, and the month was characterised by an increase in volatility and falling stock markets. The indices returned -4.7 per cent and -5.3 per cent respectively. Several areas of concern clouded markets, for example discussions regarding the potential collapse of Chinese real estate company Evergrande and its consequences. Upward price pressure continued on the back of supply chain disruptions with consumer price inflation reaching its highest level in thirteen years. Within the energy sector oil, electricity and gas prices rose significantly. Several central banks indicated during the month an easing from pandemic-era monetary support. The US 10-year treasury rate rose to its highest level since May 2021.

STRATEGIES WITHIN BRUMMER MULTI-STRATEGY

During September the trend following strategies Florin Court and Lynx contributed positively. Gains from the power sector, commodities and fixed income dominated Florin Court’s performance while commodities and FX were the largest contributors for Lynx. The long/short equity strategy Manticore navigated the month’s volatility well and generated alpha gains from both its long and short book while the newly launched long/short equity fund Kersley ended the month marginally up. Macro focused Arete lost money on equity positions and systematic equities strategy AlphaCrest made alpha losses. Long/short equity strategy Black-and-White lost money from both its long and short book. Fixed income relative value strategy Frost and machine-learning strategy Lynx Constellation delivered a marginal negative return contribution.

Following BMS’s portfolio managers redemption from Black-and-White (for more detail click here), more than half of the redeemed amount has been reallocated, mainly to Manticore and Arete. The allocation to AlphaCrest and Lynx Constellation have marginally decreased. As of October 1st, Brummer Multi-Strategy began allocating capital to the new industrials focused long/short equity strategy Pantechnicon. The initial allocation to Pantechnicon is approximately 6 per cent.