Brummer Multi-Strategy monthly commentary August 2022

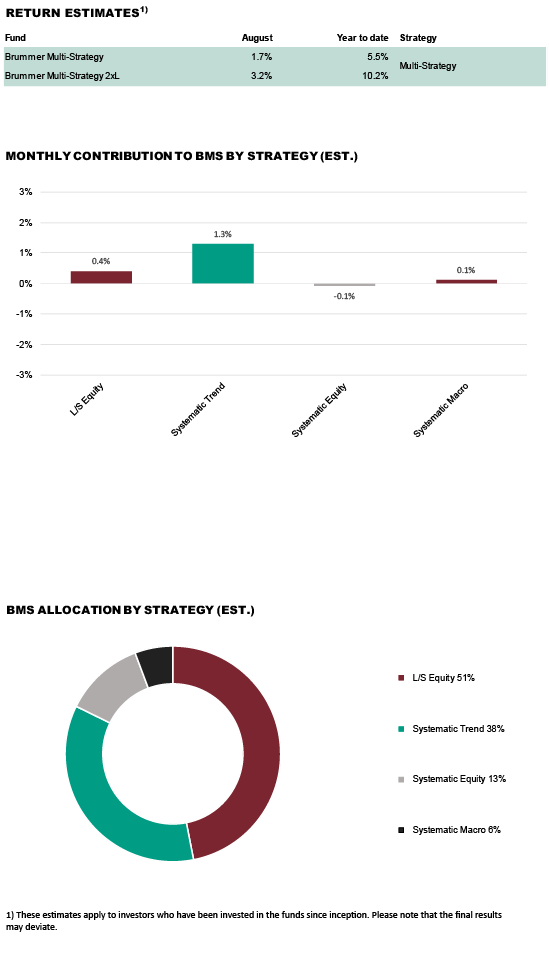

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated return of 1.7 and 3.2 per cent respectively in August (1.7 and 3.3 per cent for the corresponding USD classes).

MARKETS

In August investors across global markets faced weakening economic indicators and were once again reminded of a gloomy global outlook with high inflation, rate hikes and geopolitical uncertainty. US consumer spending slowed during the month while several housing markets showed signs of cooling as central banks remain focused on interest rate hikes in order to tame inflation. Among central banks in developed markets, the Federal Reserve signalled continued rate hikes and the Bank of England and the Reserve Bank of Australia increased rates by 0.5 percentage points. In emerging markets, the People’s Bank of China reduced lending rates following weaker than expected economic data while rates were lifted by central banks in, for instance, Argentina, Mexico and Peru. US-China geopolitical tensions increased following the speaker of the US House of Representatives visit to Taiwan. Equity markets rallied during the first half of the month following softer than expected US inflation data but this shifted to broad-based declines on the back of the Jay Powell’s hawkish speech at Jackson Hole. In commodity markets, oil prices whipsawed while natural gas prices continued higher. In fixed income markets, US bond yields moved higher and rose further after a hawkish Federal Reserve. European bonds recorded their worst month in decades with the sell-off fuelled by inflation fears and potential rate rises. Amid political and economic uncertainty in the UK the pound depreciated significantly against the US dollar, posting its steepest monthly fall since 2016 while the latter surged against a basket of currencies.

STRATEGIES WITHIN BRUMMER MULTI-STRATEGY

BMS generated positive returns in August with solid gains across most investment strategies. Trend following strategies performed well on both alternative and developed markets. Alternative market trend following was the largest contributor for the month with significant gains in power markets but also in fixed income, commodities and currencies, outpacing minor losses in credits and equites. Developed market trend following profited mainly from long positions in the US dollar and short positions in European bonds offsetting marginal losses in equities. Long/short equity strategies generated positive contribution across the majority of sectors. The largest contribution within the strategy sleeve came from global industrials with solid alpha particularly on the short side. European financials also accounted for a substantial share of the positive contribution to BMS’s performance and Nordic/European tech had a good month. The largest negative contribution came from the strategy focused on US TMT which struggled with both long and short alpha and realised losses in most sub-sectors. Systematic equity was slightly negative in August. The alternative markets systematic macro strategy performed well with gains in commodities, currencies and fixed income, outweighing losses in equities.

As of September 1st, the portfolio managers increased the allocation to alternative markets systematic macro and decreased the allocation to long/short equity in the US TMT space.