Brummer Multi-Strategy monthly commentary July 2022

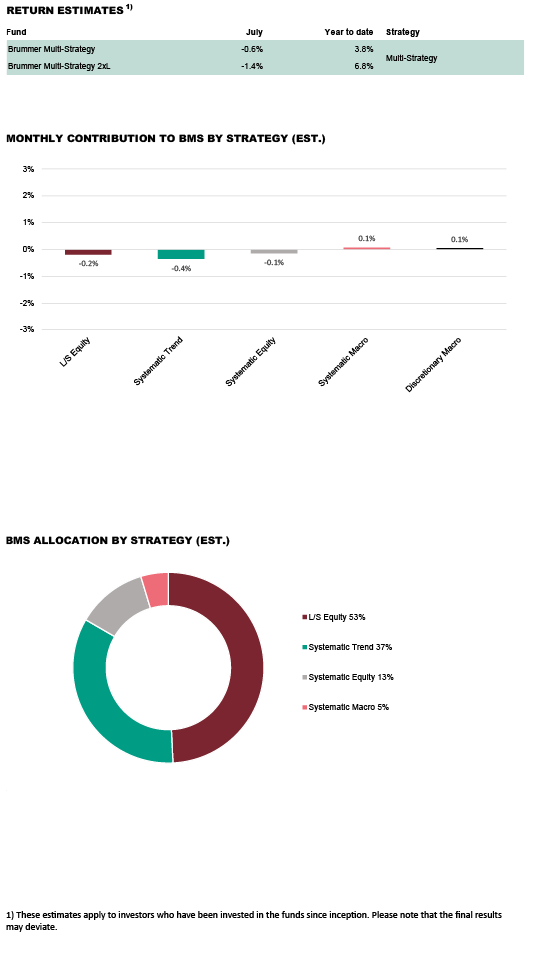

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated return of -0.6 and -1.4 per cent respectively in July (-0.6 and -1.3 per cent for the corresponding USD classes).

MARKETS

In July, data in the US and Euro area showed inflation remaining at record levels, consumer sentiment fell due to the rising cost of living and incoming economic data continued to indicate an upcoming recession. The European Central Bank followed through with its first rate hike in more than a decade, raising rates by half a percentage point along with a new bond buying program to tackle surging debt costs of governments in member states. Also, in line with expectations, the US Federal Reserve announced another 75 basis point hike for the second consecutive month. Despite the rate hike, markets interpreted dovishness in Jerome Powell comments at the Federal Open Market Committee meeting causing a surge in both equity and bond markets. Stronger than expected corporate earnings in the energy and tech sectors also helped fuel a return to risk appetite in developed market equities as both the S&P 500 and NASDAQ composite indices recorded their best months since 2020. In fixed income, Treasury markets also had their best month since 2020 with most Treasury yields falling back below three per cent driven by increasing recession fears while the US yield curve inverted. WTI and Brent crude oil prices swung around 100 dollars per barrel, mainly driven by investors rebalancing between demand and supply concerns. The acceleration of the European gas price intensified during the last week of the month as Russia decided to decrease flows from the Nord Stream 1 pipeline. In foreign exchange, the US dollar index increased to its highest level in two decades at the beginning of the month but fell thereafter as markets, among other factors, absorbed Federal Reserve’s rate hike and dovish comments from the Fed Chairman.

STRATEGIES WITHIN BRUMMER MULTI-STRATEGY

BMS ended July slightly down with mixed contribution from the investment strategies. The largest contribution came from exotic market trend following which profited mainly on long positions in power markets, but also on fx positions, which outweighed marginal losses in equities, rates and credits. The month’s largest detractor was developed market trend following with losses primarily from short positioning in European bonds and US equity indices. Performance was mixed among the long/short equity strategies, alpha on both the long and short side were realised in the European financials sector while global industrials, in particular the transportation sector, accounted for the majority of the negative contribution offsetting smaller gains in the energy sector. The long/short equity strategies focused on US TMT and the Nordic/European tech sector were flat and slightly negative respectively. Discretionary macro contributed positively, and systematic equity ended the month down. Systematic macro generated gains across all asset classes, with performance primarily driven by positions in rates and currency markets.

As of August 1st, the portfolio managers increased the allocation to systematic macro while redeeming the remaining allocation in discretionary macro.