Brummer Multi-Strategy monthly commentary May 2022

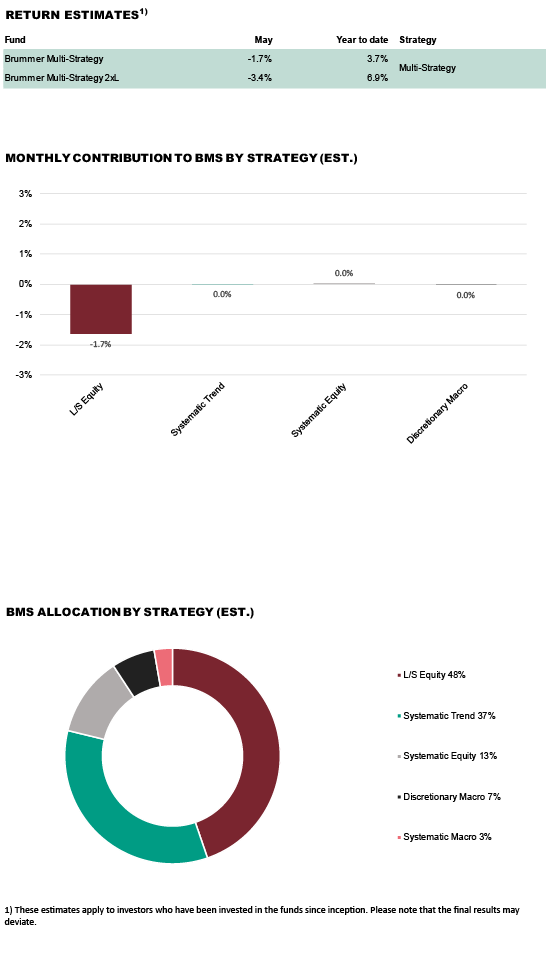

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated return of -1.7 and -3.4 per cent respectively in May (-1.7 and -3.4 per cent for the corresponding USD classes).

MARKETS

Market volatility continued in May as central bank focus remained on taming inflation amid increasing data pointing towards a potential slowdown in economic growth. In the US, the Federal Reserve raised rates by 50 basis points at the beginning of the month and signalled further hikes later this year. US yields ended the month lower, however, driven primarily by weak economic data and rising recession risks as investors priced in a less aggressive monetary policy path. In the eurozone, the ECB indicated their first rate hike in July while inflation numbers came in higher than expected causing bond markets in the eurozone to fall. Global equity markets were whipsawed by corporate earnings as turmoil persisted for technology stocks which initially continued their downward trend before rebounding somewhat during the last week of the month. In commodity markets oil prices continued higher as the EU moved towards restricting Russian oil imports and China relaxed COVID restrictions. The US dollar index appreciated to a 20-year high before falling at month-end driven by weak corporate earnings and economic data while the euro and pound appreciated.

STRATEGIES WITHIN BRUMMER MULTI-STRATEGY

Brummer Multi-Strategy finished the month in negative territory in May. Developed market trend following had another positive month profiting from fixed income and commodity positioning which outpaced losses in currency markets. Performance for long/short equity strategies was mixed with solid alpha in the financials and industrials space. The primary detractor for the month was US tech focused long/short equity which struggled with poor long alpha on the back of earnings. Exotic market trend following contributed negatively with losses in credits and fixed income overshadowing gains from power markets. Systematic equity contributed marginally while discretionary macro was essentially flat for the month, profiting from equities while generating losses in commodities.

As of June 1st, the portfolio managers marginally increased the allocation to industrials focused long/short equity and invested in a new systematic macro strategy focusing on alternative markets. The portfolio managers decreased the allocation to tech focused long/short equity and systematic equity.

For more information on Brummer Multi-Strategy's performance, please see the tables and graphs below.