Brummer Multi-Strategy monthly commentary October 2022

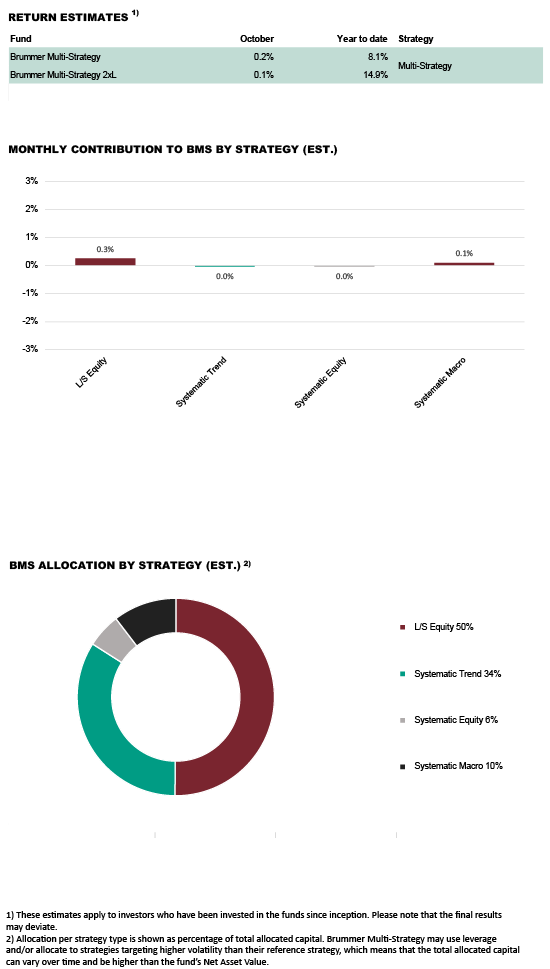

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated return of 0.2 and 0.1 per cent respectively in October (0.3 and 0.2 per cent for the corresponding USD classes).

MARKETS

Equity markets moved higher in October, apart from a particularly disappointing earnings season for several of the world’s largest tech companies, most sectors delivered stronger than expected numbers. The ECB raised interest rates by 75 basis points while Christine Lagarde’s slightly softer guidance led markets to price in less aggressive future rate hikes from the central bank. Both the euro and European bond yields fell following the ECB’s announcement. Third quarter US GDP numbers came in stronger than expected as did eurozone and US inflation numbers. In commodity markets, the price of Brent crude oil moved higher following the OPEC+ decision to cut production while the US announced it will release more oil from its Strategic Petroleum Reserve in order to stabilise markets.

STRATEGIES WITHIN BRUMMER MULTI-STRATEGY

BMS ended October in slightly positive territory. Long/short equity contributed positively with European financials generating gains from bank and insurance themes, global industrials strategies profited from solid long alpha while US TMT and Nordic/European tech strategies struggled. The contribution from trend following was mixed. Developed market trend following profited from fixed income and foreign exchange positioning, outweighing losses in commodities and equities. Alternative market trend following capitalised on fixed income, equities and commodities but these gains were offset by losses in credits, currencies and power markets. Systematic equity continued to struggle and ended the month down. Systematic macro focused on developed markets generated gains in fixed income positioning outweighing losses in commodities and equities. Alternative markets systematic macro continued to deliver positive performance, making money from relative value positions in equities, commodities and fixed income markets which compensated for losses in currencies.

As of November 1st, BMS’s portfolio managers increased the allocation to alternative markets systematic macro and European financials long/short equity, while the allocation to systematic equity was decreased. Intra-month (October), the portfolio managers also decreased the allocation to developed market trend following.