Brummer Multi-Strategy monthly commentary September 2022

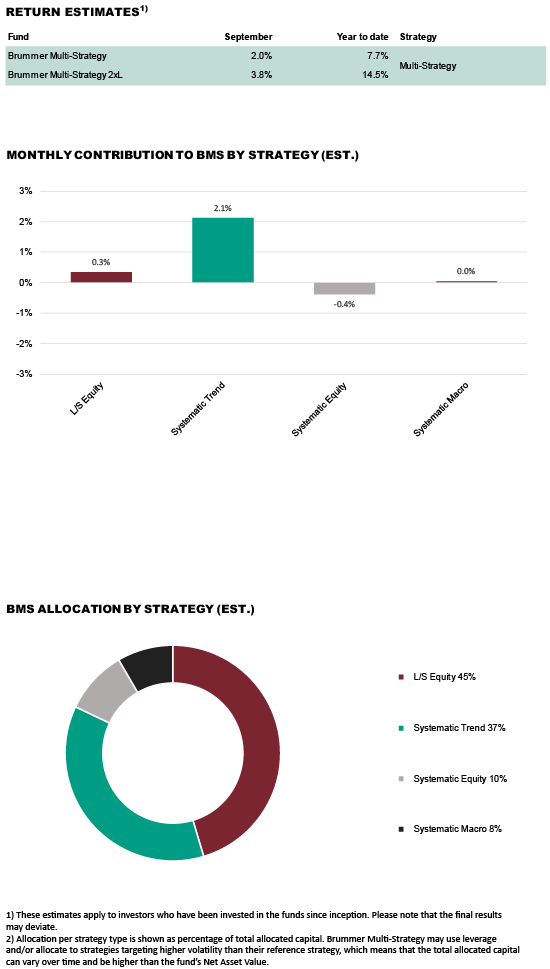

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated return of 2 . 0 and 3. 8 per cent respectively in September ( 2.1 and 3. 9 per cent for the corresponding USD classes).

MARKETS

September saw rate rises from global central banks with both the Federal Reserve and the ECB raising rates by 75 basis points. Global equity markets fell during the month with US stocks posting a third consecutive quarterly loss for the first time since the financial crisis of 2008. In fixed income markets, yields rose on the back of higher than expected inflation numbers, UK 10-Year Gilt yields rallied in particular following the announcement of the government’s latest fiscal plan. In currency markets, the dollar continued its move higher with the British pound falling to an all-time low against the greenback, the euro to a 20-year low and the yuan to its lowest dollar exchange rate since 2008. Japan, now the only country with negative interest rates, intervened in currency markets to stem the fall in the yen against the dollar. Geopolitical tension in eastern Europe intensified as Russia announced partial mobilisation and escalation of the war in Ukraine, fuelling the energy crisis and concerns over Europe’s energy supply this winter. In commodity markets, oil prices retreated somewhat falling to its lowest level since January reflecting concerns about the global economic outlook.

STRATEGIES WITHIN BRUMMER MULTI-STRATEGY

In September, BMS had another good month with most investment strategies contributing positively. Developed market trend following was the largest contributor for the month, profiting in particular from long dollar and short European bond positioning while commodities detracted slightly. Alternative market trend following also had a solid month, profiting from strong upward trends in fixed income and a stronger dollar against emerging market currencies which outpaced losses from the power sector. Long/short equity strategies navigated the month well realising short alpha gains across US TMT, European financials, and Nordic/European tech while global industrials finished the month slightly negative. Systematic equity had another negative month with negative alpha. The alternative markets systematic macro strategy posted positive performance with gains in equities and currencies while fixed income positioning finished flat and commodities detracted somewhat.

As of October 1st, the portfolio managers started allocating capital to a systematic macro strategy focused on developed markets and decreased the allocation to systematic equity.