Brummer Multi-Strategy monthly commentary March 2023

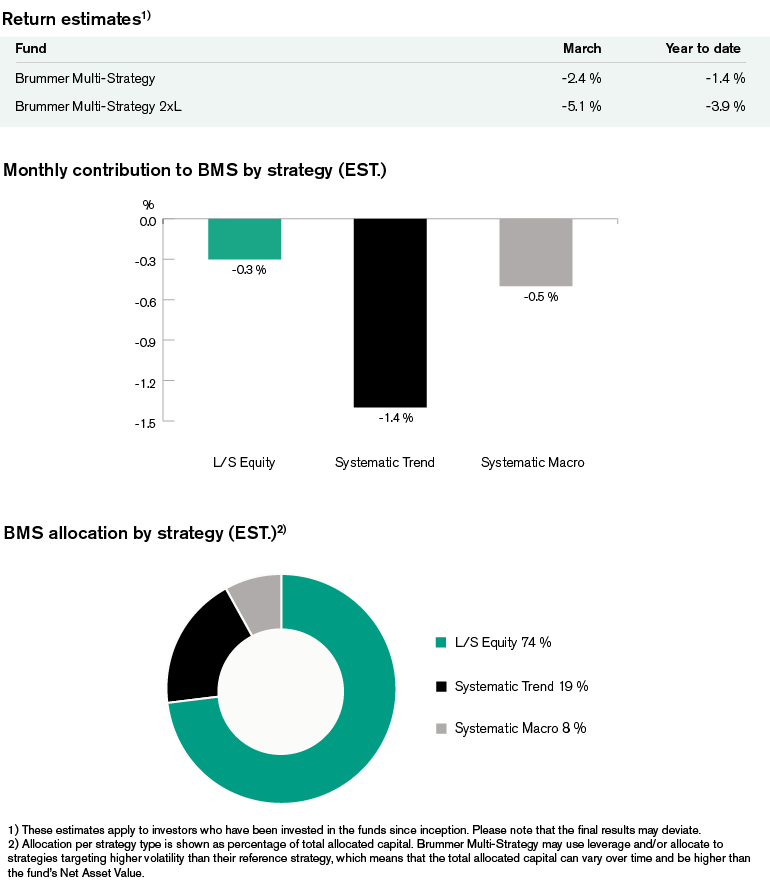

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated return of -2.4 and -5.1 per cent respectively in March (-2.2 and -4.9 per cent for the corresponding USD classes).

Markets

March picked up where February left off with markets anticipating rates remaining higher for longer amid data pointing to resilient economies, persistent inflation and hawkish rhetoric from central banks. Sentiment made a U-turn, however, as turbulence created by the collapse of Silicon Valley Bank and other regional lenders as well as the forced acquisition of Credit Suisse by its chief rival UBS led investors to re-price the future rate path of central banks. The turmoil was particularly acute in fixed income markets with the 2-Year US Treasury yield experiencing the largest 1-week move since 1987. In contrast with bond traders, equity investors remained relatively calm and once the banking crisis seemed to be contained within a smaller group of (potentially mismanaged) banks, focus turned to lower interest rates and equities staged an impressive comeback. Especially large-cap growth outperformed. In commodity markets the price of gold moved significantly higher following the banking crisis while Brent and WTI crude oil prices fell during the first half of the month before rebounding toward month-end.

Strategies within Brummer Multi-Strategy

BMS generated negative returns in March. Losses came primarily from systematic trend-following given the extreme trend reversals during the month with short bond positioning particularly costly. Long/short equity strategies generally held up well during the month given the market volatility with strong long alpha in US TMT and solid short alpha in global industrials contributing positively. European financials struggled, however, with aggressive deleveraging across the sector with stock performance driven to a large extent by factors other than fundamentals. Positions in global health care and Nordic/European tech also detracted marginally from performance. Systematic macro generated gains in equity positioning but these were outweighed by losses in relative value positioning in foreign exchange and rates.

The portfolio managers decreased the allocation to systematic trend intra-month in March. As of April 1st, BMS’s portfolio managers decreased the allocation to systematic macro.