Brummer Multi-Strategy monthly commentary August 2024

Brummer Multi-Strategy (BMS) USD and Brummer Multi-Strategy 2xL (Bermuda) USD posted an estimated return of 0.1 and -0.1 per cent respectively in August.

Markets

This August, investor patience was tested across markets as turbulence initially flooded markets. Equity markets were jolted on a global scale as a relatively significant increase in Japanese interest rates led to an unwind of yen carry trades, in which investors rushed to sell off assets held in the currency thus causing a significant drop in Japanese equity indices such as the Nikkei 225 and TOPIX. This sell-off, in tandem with a recession scare in the US brought on by weak jobs and manufacturing reports, caused ripple-effects across equity markets resulting in a record spike in the VIX and large drops due to widespread risk-off positioning. These recession qualms were eventually satiated as US inflation came in below consensus, and as the Fed chair Jerome Powell announced that “…the time has come for policy to adjust” at the Jackson Hole summit, all but confirming rate cuts in September. Ultimately, US and continental European equity markets ended the month on a positive note while UK and Japanese stock markets ended roughly flat. The prospect of US rate cuts caused the yields on US treasury bonds to move lower while European bond yields ended flat for the month as investors await the next move from the ECB. The certainty of US rate cuts paired with uncertainty of cuts elsewhere caused the US dollar to significantly weaken against various currencies, in particular the euro and British pound. Following a rocky month due to geopolitical worries, oil prices ultimately moved lower for the month while gold continued to appreciate, becoming the top-performing major asset YTD.

Brummer Multi-Strategy

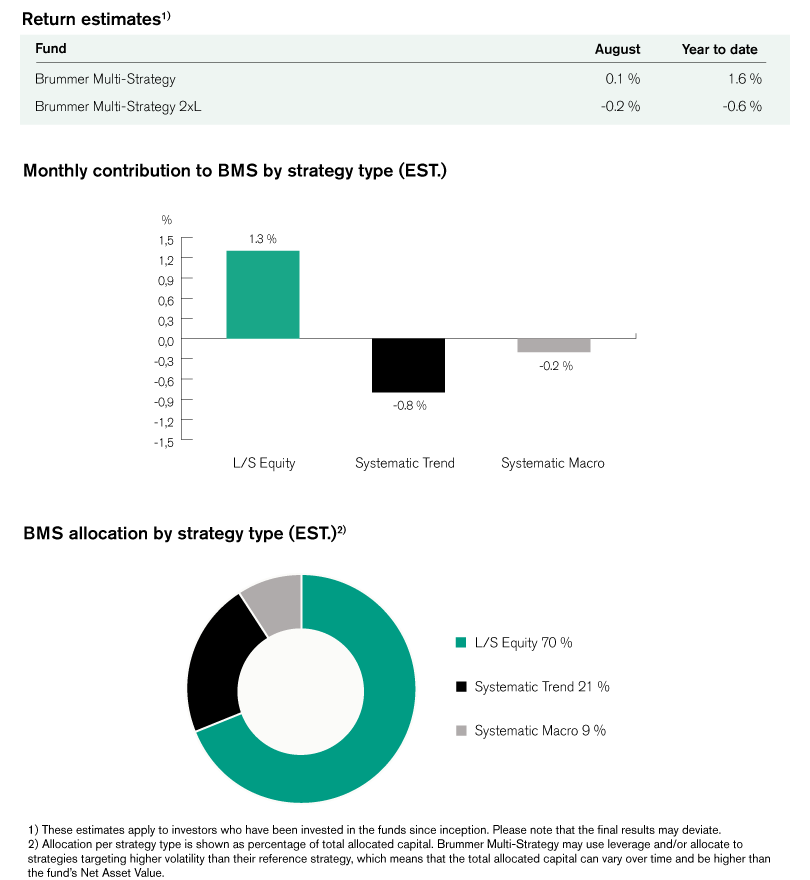

In August, systematic trend following strategies struggled given the choppy market environment. On developed markets, long exposure in the US dollar proved costly as well as positioning in equities and commodities. These were partially offset by profitable positioning in fixed income. In alternative markets, profits made in commodities were offset by the remaining sectors: power, fixed income, FX, and equities.

Within the long/short equity bucket, all underlying strategies contributed positively this month. In the US TMT sector, solid alpha gains were realized within the following sectors: semiconductors, financial services, and software & services which were lightly offset by detractors in media & entertainment. In global healthcare sectors, solid gains were attributable to positioning in pharmaceuticals, biotech, and life sciences. European financials were slightly positive for the month.

BMS’s systematic macro strategies diverged from one another somewhat in August, ultimately detracting for the month. On developed markets, losses within FX, equities and commodities were partially offset by positioning in fixed income. On alternative markets, gains in commodities and FX were partially offset by losses in fixed income.

As of September 1st, BMS’s portfolio managers decided not to rebalance the risk in the portfolio in any significant way.

For more information on Brummer Multi-Strategy's performance, please see the tables and graphs below.

This is marketing communication. Read the fund's information memorandum and key investor document (KID) before making any definitive investment decisions.