Brummer Multi-Strategy monthly commentary April 2024

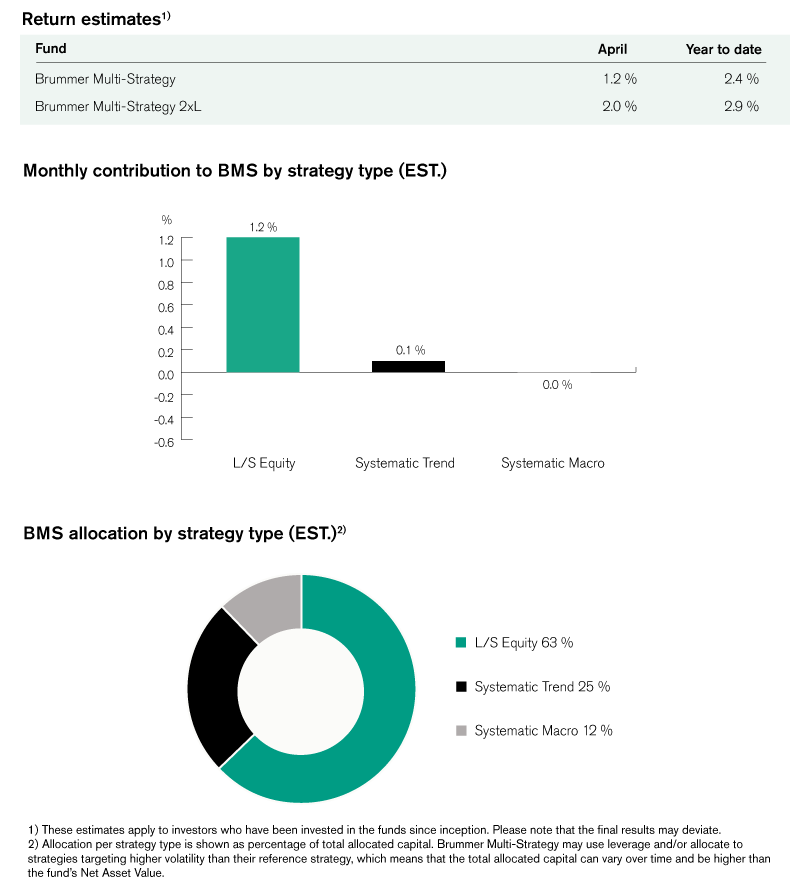

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated return of 1.2 and 2.0 per cent respectively in April (1.4 and 3.3 per cent for the corresponding USD classes).

Markets

April was a turbulent month for markets as fears of US stagflation and further geopolitical turmoil resonated across the globe. US equities saw a rather steady decline over the month on the back of inflation rising and Q1 growth stagnating, far above and slightly below expectations respectively. Some losses were recouped at the tail-end of the month as mega-cap names provided strong Q1 earnings reports. In Europe, equity performance was mixed as the Stoxx Europe 600 index moved lower in spite of dovish ECB comments while the FTSE 100 ended the month higher as domestic PMIs exceeded expectations. Following a record setting March, the Nikkei 225 took a tumble this month, in large part fueled by a weakened yen. US inflation figures solidified expectations of a delay in rate cuts leading US treasury yields sharply higher dragging German Bunds and UK Gilts up with them. The US dollar also strengthened during the month, as markets expect the Fed to lag behind other central banks when it comes to cutting rates. Events in the Middle East once again left a mark on commodity markets leading to a spike in oil prices although this was later tempered by increased US supply. The easing of tensions towards the end of the month made its mark on the price of gold, as its steep rally tapered off.

Brummer Multi-Strategy

Trend following strategies ended marginally positive for the month. In alternative markets, profitable positioning in fixed income was to a large extent offset by losses stemming from credit and equity positions. FX and fixed income positioning proved to be the most profitable asset classes in developed markets but was largely offset by losses in equities and commodities.

Long/short equity delivered solid alpha contribution to BMS in April. The US TMT sector proved particularly profitable, with solid short alpha across sectors which was marginally offset by positioning in mega cap tech names as well as financial services and real estate. Across the Atlantic, European financials enjoyed another strong month attributable to the banking sector as well as some names in the diversified financials space. Positioning in the healthcare sector ended roughly flat for the month, as profitable shorts in pharmaceuticals were offset by detractors in healthcare equipment. In the global industrials sector, profits were primarily driven by names in the capital goods and materials sectors.

The contribution from the systematic macro strategies were flat for the month. In developed markets, gains from fixed income and FX were partially offset by commodity positions ultimately ending on a positive note. These profits were however offset by positioning in alternative markets, where fixed income and equities proved to be the main detractors.

As of May 1st, BMS’s portfolio managers decreased the allocation to the systematic trend-following and systematic macro strategies. Within the trend-following bucket, the exposure to alternative markets decreased while in developed markets the allocation was marginally increased. In the market neutral long/short equity bucket, BMS will going forward no longer allocate any risk to the strategy focusing on the industrials sector. Later this year, BMS will start allocating risk to at least two new strategies. The first one is expected to be included in the portfolio as of late Q2.

This is marketing communication. Please refer to the prospectus and to the KIID/KID of the relevant fund before making any final investment decisions.