Brummer Multi-Strategy monthly commentary March 2024

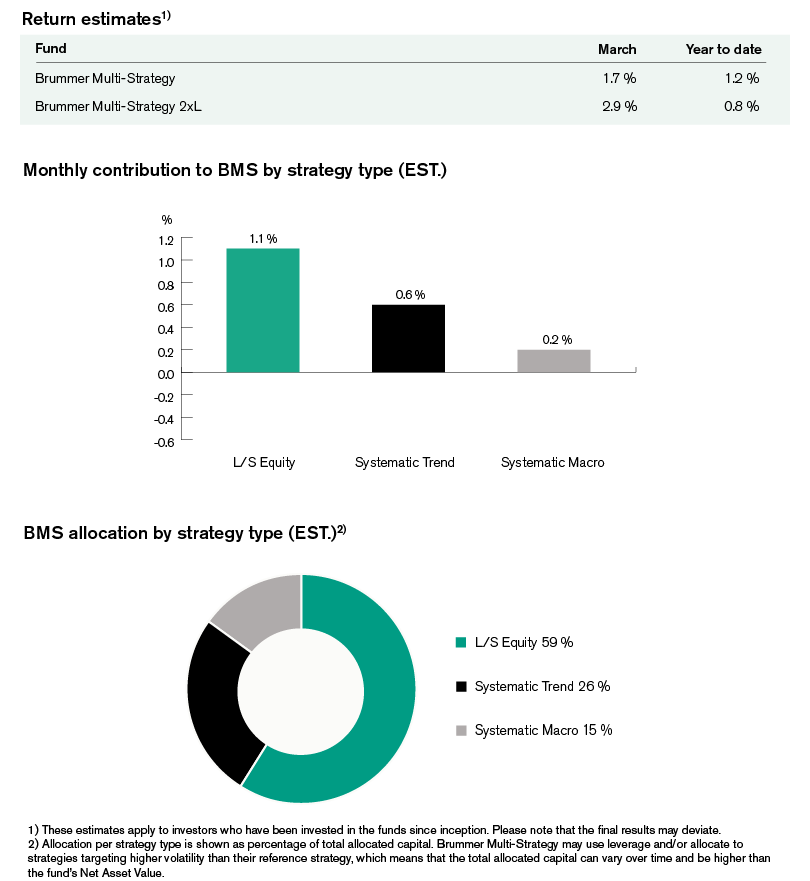

Brummer Multi-Strategy (BMS) SEK and Brummer Multi-Strategy 2xL (BMS 2xL) SEK posted an estimated return of 1.7 and 2.9 per cent respectively in March (1.9 and 3.1 per cent for the corresponding USD classes).

Markets

In March, developed market equities posted another strong month despite mixed macro-economic data. On the European front, the Euro Stoxx 600 and FTSE 100 rallied on the back of strong economic data, bolstered by sentiment that the ECB and BoE would stick to plans to lower rates during the year. The US was marked by uncertainty, as a hotter-than-expected core CPI print lowered expectations for the pace of rate cuts in 2024, cooling performance somewhat. The S&P 500 did however, ultimately end on a strong note for the month as the Fed indicated it still expects to cut rates three times during the year. On the other side of the Pacific, the Nikkei 225 crossed into new territory, breaching the 40,000 mark as the BoJ decided to end its yield curve control and exit its long period of negative rates. The uncertainty of policy rates in the US left an impression on its Treasury yields as the 2- and 10-year yields rallied, only to be offset by the Fed easing concerns over the pace of rate cuts, ultimately ending slightly up for the month. On the other side of the pond, European yields saw a steady decline on the back of optimistic sentiment and strong economic data. In currency markets, March saw the US dollar appreciating against a basket of currencies while the Japanese yen moved lower in spite of the BoJ exiting its negative interest rate policy. Reports of a potential ceasefire in the Middle East partially offset reports of OPEC+ constituents extending their production cuts as oil prices moved somewhat higher. March also saw gold and other metals ending on a high note.

Brummer Multi-Strategy

Trend following strategies contributed solidly to performance this month. In alternative markets, modest gains generated from positioning in credit, FX and equities were partially but not entirely offset by short positions in power. Trend following in developed markets had yet another successful month this year, as positions in equities, FX and commodities generated solid profits.

Long/short equity provided the largest contribution to performance in March. In the US TMT sector, with strong profits across sectors on both the long and short-side, with software, consumer discretionary and semiconductors serving as standouts. European financials enjoyed solid gains within the banking theme, which was partially offset by positions in insurance companies. Alpha in the healthcare sector contributed positively to performance this month with pharmaceuticals performing the best. Global industrials generated profits from the energy and transport sector, which were partially offset by short positions in capital goods and automobiles.

Systematic macro contributed slightly in March, mainly driven by positioning in fixed income and commodities in alternative markets. These losses were partially offset by profitable positions in developed markets, where long positioning in commodities and FX generated the most gains.

As of April 1st, BMS’ portfolio managers slightly increased the risk allocation to the novel strategy operating in the US TMT and consumer discretionary sectors, decreasing the risk allocation to global industrials and European financials somewhat.

This is marketing communication. Please refer to the prospectus and to the KIID/KID of the relevant fund before making any final investment decisions.